Economic Models: Aggregate Supply and Aggregate Demand

Macroeconomic models are based on the fundamental relationships among households, businesses, and financial markets. An economic model describes how the economy changes over time in terms of a few key variables, such as the unemployment rate, inflation, interest rates, aggregate supply and aggregate demand. Microeconomic models describe supply and demand in terms of quantity and price, how one changes in response to the other, all relevant factors being equal, or as economists are fond of saying, ceteris paribus. Macroeconomic models, on the other hand, model how several key variables, such as interest rates and inflation, affect consumers and firms in the aggregate. Because there are millions or billions of economic agents, macroeconomic models depend on statistics. Econometrics is a branch of economics using statistics to study economic models and data.

Models don't explain everything. Instead, models focus on a few key variables that can be effectively modeled, so that the predictions of these models can be tested empirically. This resembles scientific hypothesis testing, where 2 experiments are conducted, where the only differences between the 2 experiments is a difference in the control variable. By changing only the control variable and examining the results, the importance of the control variable and its effects can be studied. It is not possible to run controlled experiments on the economy, since economists obviously do not control the economy. Therefore, economic models are the next best thing, but like control experiments, they are simplified, so that the effects of key macroeconomic variables and their interrelationships can be better understood.

The income received by households from businesses is either spent for consumption or saved. Consumption is the buying of products and services provided by businesses, so money spent for consumption is returned to businesses, so that they can pay for the capital and labor used to produce the product or service. This payment provides the income for households. Moreover, most households save some of their income by using the services of financial markets, which, in turn, provides investment funds for businesses.

Within the context of an economic model, economic shock is defined as a major disturbance that originates outside of the model, that is not predicted by the model. Since many macroeconomic variables are unpredictable, they cannot be incorporated into a model, but a model can be designed to study the impact of such changes. Unpredictable macroeconomic variables include changes in consumer and business confidence, changes in monetary or fiscal policies, or changes in key inputs to the economy, such as the quantity and prices of energy.

There are 2 main types of variables: endogenous and exogenous variables. Endogenous variables are included in the model, as inputs or outputs or both, and the model accounts for changes in these variables. By contrast, exogenous variables occur outside the model. Although exogenous variables are unpredictable, the model does try to account for how the endogenous variables will change in response to changes in exogenous variables. All economic shocks are exogenous variables.

Multiplier Effect

Economic models must account for the money multiplier effect, which is a magnifying effect that time has on any increase or decrease in aggregate demand. This multiplier effect exists, because money has velocity. The expenditure of one person is the income for another. Hence, expenditures have a multiplier effect, which is an endogenous variable. If $100 is spent, then someone receives at $100 as income, who then also spends that extra income. However, on average, the entire amount is not spent. To simplify economic analysis, the multiplier is assumed to be a fixed percentage. So, if a consumer receives $100, then spends $50 and saves the remaining $50, then the propensity to consume is 50%. By following the subsequent transactions after the initial expenditure of $100, the total expenditures equal the following:

$100 + $50 + $25 + $12.50 + $6.25 + … = $200

This geometric series can be calculated using the formula:

Increase in Aggregate Demand = Amount Spent / (1 − Marginal Propensity to Consume)

Example: $100 / (1 − 0.5) = $200

So, the multiplier is 2, because an initial $100 purchase yields a $200 increase in aggregate demand. The multiplier effect is not constant. If the economy is below its equilibrium, then the SRAS curve will be relatively flat, which will yield a higher multiplier, because economic output can increase without substantially increasing aggregate price levels. If economic output is above its equilibrium position, then the SRAS curve will move sharply upward into a vertical position, where the multiplier effect will be much smaller or nonexistent, because the aggregate price level will increase sharply even with small increases in economic output, as the economy strains its resources to increase output.

Diagram showing how increases in aggregate supply and economic output becomes less for the same given change in aggregate demand as real GDP approaches, then surpasses, potential GDP. (P = Price, AD = Aggregate Demand)

Macroeconomists often divide the aggregate supply curve into 3 sections.

- The 1st section is the fixed price level range, where quantities can be increased without increasing inflation, since the economy is below its potential output. (Example: AD1 to AD2 in the diagram.)

- However, as potential output is approached, then prices start rising faster as quantities are increased further. (Example: AD3 to AD4 in the diagram.)

- Prices rise fastest and real GDP grows slowest, when economic output exceeds potential output. The economy can temporarily produce more than its potential output, by investing more capital, by running factories longer, and by increasing overtime, but it will eventually return to its equilibrium state of potential output. Hence, this part of the curve is vertical, where increasing aggregate demand simply results in greater inflation. The cost of raw materials and labor rises steeply, forcing businesses to raise their own prices. (Example: AD5 to AD6 in the diagram.)

AD-AS Economic Model

The 3 main endogenous variables in most macroeconomic models is the real interest rate (r), economic output (Y), and aggregate price levels (P). An important macroeconomic model is the Aggregate Demand-Aggregate Supply Model, otherwise known as the AD-AS model. The 2 main exogenous variables in the AD-AS model are aggregate demand and aggregate supply. The AD-AS model charts economic output and price levels with changes in aggregate demand or aggregate supply. For instance, if aggregate demand changes, then the AD-AS model will attempt to predict price levels and economic output changes in response, but the model does not explain why the change in aggregate demand occurred, only the consequence of the occurrence.

Aggregate supply and demand differs from the supply and demand experienced by a firm. Microeconomic supply depends on relative price, with other things being equal. Aggregate supply reflects aggregate price levels, which is the overall level of prices in the economy.

Changes in aggregate demand or aggregate supply may occur for many reasons, such as changes in consumer and business confidence, or changes in government purchases, or it could even be caused by increasing debt, such as that which has occurred in the 2007 - 2009 Great Recession. Macroeconomists, of course, are interested in why these events occur, but because they are not predictable, these exogenous variables cannot be modeled.

Modeling Responses to Economic Shocks

An economic shock is a sudden and large change in an exogenous variable.

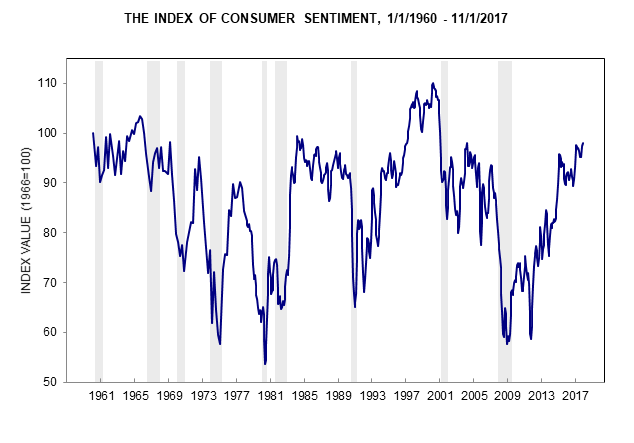

Demand-side shocks are exogenous variables that include changes in consumption, investment, including government consumption or investment, or net exports. Increases or decreases in consumer or business confidence will obviously influence aggregate demand. There are several websites that provide measures of confidence. Several economic indicators, including indexes of consumer confidence and measures of CEO confidence, can be found at The Conference Board. The Surveys of Consumers conducted by the University of Michigan also provides an Index of Consumer Sentiment and an Index of Consumer Expectations, which also shows changes from the previous month and the previous year.

Shaded gray areas depict recessions. Note how consumer sentiment declines right before recessions, and increases right after recessions.

Source: Surveys of Consumers

Supply-side shocks include sudden changes in the price of inputs, especially energy, since energy is needed to produce any product or service.

How the AD-AS Economic Model Describes Changes to Equilibrium after an Economic Shock

Empirically, it has been observed that aggregate prices do not fall often. Even if the economy slows considerably, businesses expect the government to stimulate aggregate demand through fiscal or monetary policies. But if the slowdown lasts long enough, then businesses will be forced to lower prices to reduce their inventory and to make better use of their capital.

If aggregate demand increases, and the economy is at less than potential output, then aggregate supply will move along the SRAS curve without a significant increase in prices. However, if economic output is already at its natural output, then aggregate supply will shift along the SRAS curve to a temporary equilibrium, at higher prices and higher economic output. However, economic output will eventually fall back to its natural rate, commensurate with the natural rate of unemployment, as prices rise further, when the economy has enough time to respond fully to the increased aggregate demand.

Aggregate supply adjusts more slowly than aggregate demand, because most businesses will increase inventories or increase production rather than raise prices to meet increasing demand, especially because there are menu costs in changing prices. However, menu costs may become less significant as technology reduces the time and cost of changing prices, such as using flat-screen TVs to display menus. And in the online world, prices can be changed instantly, not only depending on the cost of inputs, but also what the seller knows about the buyer. For instance, Amazon.com may show higher prices to people who subscribe to their Amazon Prime program, since subscribers are more likely to buy from Amazon because of their membership.

Exogenous Variables Affecting Aggregate Demand and Aggregate Supply

As previously stated, AD-AS models do not predict changes in exogenous variables; they only predict how the economy will respond to changes to those variables. The most prominent of these variables are changes in consumer or business sentiment or confidence, changes in fiscal policy and monetary policy, changes in expectations about future income, taxes, or inflation, a redistribution of income, and foreign exchange rates.

Consumer and Business Confidence

When consumer or business confidence declines, savings increase. Since more income is devoted to savings, less income is spent for consumption, thereby decreasing aggregate demand. Since the economy takes time to respond, price levels decline, but not as much as they would in the long run. Meanwhile, economic output declines below its natural rate. The increase in savings results in a paradox of thrift, because in the short run, increases in savings decreases consumption, thereby decreasing economic output.

Eventually, an increase in savings will increase investments in capital, eventually yielding higher output. Potential GDP increases because of the increased capital, facilitated by increased consumption resulting when household wealth increases, via the savings, and from pent-up demand. As the economy gets better, consumer and business confidence increases, along with economic output. Additionally, aggregate price levels are lower, which also stimulates aggregate demand.

Confidence levels react to the economy as well as act upon it. Moreover, changes in consumer and business confidence or sentiment can be self-fulfilling. If confidence declines, then aggregate demand will decline along with it, which, in turn, will decrease confidence even further. Likewise, when confidence increases: aggregate demand increases, which further increases business and consumer confidence. However, the reinforcing decreases or increases are self-limiting.

Aggregate demand will only fall so low. People still need to eat, pay for housing, medical care, and other necessities of life. While some decisions can be delayed, this delay only adds up to the pent-up demand that will cause the aggregate demand to increase later. Aggregate demand also has its upper limits, especially in the short run, since the economy can only produce so much, given the resources at the time.

Expectations of Future Income, Prices, and Inflation

Expecting a higher future income, business people will increase investments and consumers will spend more and save less. Expectations of a lower future income will have the opposite effect, causing businesses to decrease investments and for consumers to save more by spending less.

High expectations for the future are important for both consumer and business investments, but the difference between low and high expectations for business investments will exceed that for consumer investments, and likewise, the volatility of business investments exceed that for consumer saving. Consumers tend to save less and spend more, as consumer confidence about the future increases, and if the future turns out to be less than expectations, consumers can easily change their consumption. On the other hand, a certain time commitment must be made on business investments, since such investments tend to take months or years to realize, such as the building of a new factory. So the marginal product of any new investment will have to be determined when the investment is completed. Of course, projections over a longer time frame will the less accurate than for the short-term, which is why business confidence will depend more on informal projections, what John Maynard Keynes called "animal spirits."

Expectations of higher inflation will also cause people to spend more now, since their money will be worth less in the future. If lower inflation is expected, or even deflation, then people will save their money by spending less now, since they anticipate that their money will be more valuable in the future. Indeed, deflation is a major reason why the Japanese economy has been in the doldrums for so long. The Japanese are saving instead of spending, because they are not only earning interest, but the money itself becomes more valuable by the deflation rate.

Government Policies

Government policies can also affect aggregate demand by increasing or decreasing spending, taxes, or the money supply. These types of policies are often called macro policies. A macro policy is the deliberate shifting of the aggregate demand curve to influence the level of incomes in the economy. There are 2 types of government policies: fiscal and monetary policy. Fiscal and monetary policies affect aggregate demand in the short run: long-run aggregate demand is unaffected.

Fiscal Policy

Fiscal policy guides government budget decisions: how much is spent on what programs and how to finance the expenditures, either by increasing taxes or by borrowing, thus increasing the deficit. Legislators determine fiscal policy, which, in the United States, is Congress. Extensive government borrowing reduces savings available for capital formation, but it also increases aggregate demand.

An expansionary fiscal policy either expands government spending or reduces government taxes, in which case, it is the consumers and businesses that increase spending. Businesses will also increase investments because they will get to keep more of the returns from those investments, thus increasing the marginal product of capital.

A contractionary fiscal policy has the opposite effect: government spending is reduced, which reduces aggregate demand through the government expenditures component, or taxes are increased, thereby reducing the disposable income available to consumers and businesses, which will reduce their spending. In either case, aggregate demand declines. Likewise, business investments decline because they keep less of any returns on investments, thereby decreasing the marginal product of capital.

A redistribution of income will also affect aggregate demand. Changes in income distribution can be affected by changes in government transfer payments, such as with Social Security or Medicare, or by changes in tax rates. Poor people spend more of their money, because they need to buy necessities. Rich people tend to save more of their money, because they already have everything they need to live comfortably, so they spend a lower proportion of their income. So, a redistribution of wealth from the poor and middle-class to the wealthy will have a negative effect on aggregate demand, and, therefore, on economic output. So, the most effective way to stimulate the economy with tax cuts is to give most of the tax cuts to the poor and middle-class.

Monetary Policy

Monetary policies, which are usually conducted by central banks, can also be expansionary or contractionary. Like expansionary fiscal policies, expansionary monetary policies increase aggregate demand, while contractionary monetary policies have the opposite effect. An expansionary monetary policy stimulates aggregate demand, usually by expanding the money supply or decreasing interest rates. To cool the economy, central banks decrease the money supply or increase interest rates.

The Federal Reserve of the United States, for instance, expands the money supply by buying U.S. Treasuries from its primary dealers. The Federal Reserve pays for those Treasuries by incrementing the accounts of the primary dealers by the amount of the purchase. This is how the Federal Reserve creates money. When the Federal Reserve contracts the money supply, it sells U.S. Treasuries to its primary dealers, debiting their accounts by the amount of the purchase. Increasing or decreasing the accounts of the primary dealers has a ripple effect on the economy, because their increased or decreased buying power will affect the other economic agents with whom they do business, which will, in turn, affect still more parts of the economy, thereby increasing or decreasing aggregate demand. This is the multiplier effect.

The effect of changing interest rates depends on the nominal interest rate and the demand for money. Consumers and businesses must maintain some liquidity, so that they can buy things and pay debt. Money has the highest liquidity, since it serves as the unit of exchange. Stocks and bonds and other financial instruments are not nearly as liquid, since they cannot be used as a means of payment. Although they can be converted into money, the conversion may have undesirable consequences, such as suffering losses.

The nominal interest rate affects the demand for money. Holding money incurs an opportunity cost equal to minus the inflation rate, so if the nominal interest rate is high, then the holder of money forfeits the interest that could otherwise be earned if it were saved or invested. If the nominal interest rate is low, then people save less and spend more, both because the opportunity cost of holding money is lower and because borrowing money is less expensive.

Nominal Interest Rate = Real Interest Rate + Inflation Rate

The opportunity cost of holding money is the nominal interest rate. The return of holding money is minus the inflation rate.

Return of Holding Money = − Inflation Rate

The greater the nominal interest rate, the greater the opportunity cost of holding money, which is why they are inversely related.

The Federal Reserve controls the interest rate by controlling the federal funds rate, which is the interest rate banks charge each other for loans of very short duration. Usually, the Federal Reserve sets the federal funds rate as a range rather than a specific value, such as from 0.25 to 0.5%, then increases or decreases the money supply to achieve that rate.

International Demand

International supply and demand will also affect the domestic economy. There is an international effect of domestic prices: as the price level in the domestic economy falls, assuming the exchange rate does not change, then the international demand for those goods will increase, and vice versa.

Foreign income changes will change demand for domestic goods, which will also affect the domestic economy, since richer foreigners buy more imported goods.

Foreign exchange rates will also affect aggregate demand. If the domestic currency becomes less valuable relative to foreign currencies, then foreign demand for domestic products will increase; if the domestic currency becomes more valuable, then obviously foreign demand will decline.

Interest rates can also change net investments, the amount of foreign investments in the domestic economy compared to domestic investments in foreign countries or assets. Lower domestic interest rates cause people in the United States to invest outside of the country for a higher rate of return, and, for the same reason, foreign investment is reduced in the United States. This lowers the value of the dollar against other currencies, causing imports to be more expensive and exports to be less expensive. Increasing domestic interest rates has the opposite effect.

Conclusion

The AD-AS model assumes there is an economic output equilibrium, where, if short-term disturbances moved the economy away from that equilibrium, then corrective forces will move the economy back toward equilibrium over the long run. Shocks to the economy can come from the supply or demand side. Major shocks have already occurred to the United States economy.

Both demand and supply shocks occurred during the Great Depression. On the one hand, aggregate demand declined because the great stock market crash in 1929 devastated consumer and business sentiment. The government made it worse by contracting the money supply when it should have expanded the money supply. On the other hand, the aggregate supply of crops also decreased because of the severe drought in the Midwest, made worse by poor farming practices and water mismanagement, which promoted soil erosion by wind, creating such great clouds of dust that it became known as the Dust Bowl.

In the 1970s, the OPEC countries limited the supply of oil and natural gas, causing the prices of both to spike. Not only did this reduce economic output, but it also temporarily moved the natural economic output leftward, since the economy cannot produce as much as it previously could with cheap energy.

Eventually, the economy recovers from both aggregate supply and aggregate demand shocks. Government officials learn how to manage the economy better; bad natural conditions, such as in the Dust Bowl, eventually end, and technology learns to compensate for supply shocks. Thus, the demand for energy declined as technology provided greater energy efficiency and provided the means to extract new sources of energy, such as fracking. So, in the long run, yes, we are all dead, but at least the economy keeps growing!