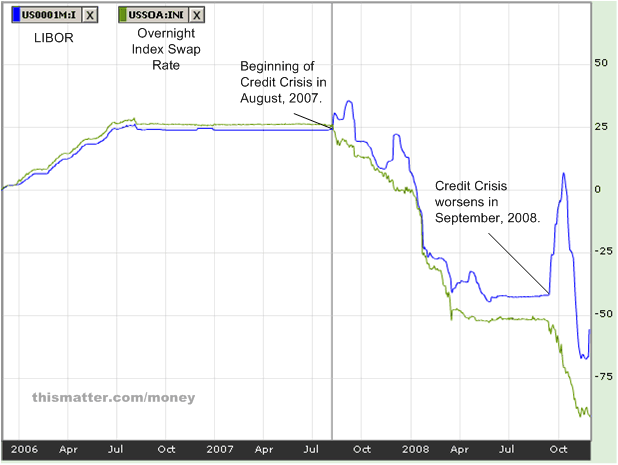

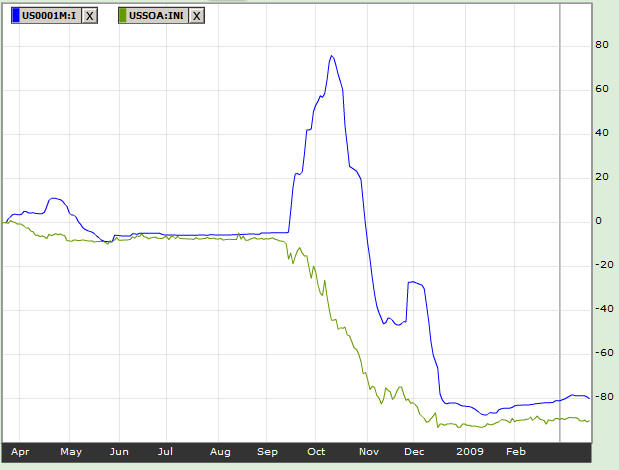

LIBOR-OIS Spread

The LIBOR-OIS spread is the difference between the LIBOR and the overnight index swap rate, that indicates credit risk in the interbank lending market. Generally, both the LIBOR and the OIS rates decline with central bank interest rates, but when lending banks are uncertain of the creditworthiness of borrowing banks, higher interest rates are charged as compensation for the higher credit risk. The LIBOR-OIS spread indicates credit risk in the interbank lending market better than the LIBOR itself because the LIBOR is also influenced by the rates set by central banks, whereas the overnight index swap rate is based only on the rates set by central banks, so subtracting it from the LIBOR yields the credit premium being charged for the higher risk.

Why a High LIBOR-OIS Spread Indicates a Limited Availability of Credit

Banks must have a minimum of reserves to conduct their business. During the course of the day, they may receive or pay out more money than expected. Depositors, for instance, may make big deposits or big withdrawals — banks can't know ahead of time what the net demand will be, hence, they need to keep a minimum of cash to service customers. However, banks don't want to keep more than they need, because cash kept in vaults doesn't earn any interest, and, reserves held in central banks pay little or no interest. So banks with excess funds lend to banks needing funds. When this interbank lending market declines because of higher interest rates, then banks are forced to hold more cash to conduct business; hence, they lend less, not only to other banks, but also to consumers. Less lending means there is less money in the economy, which lowers demands for products and services, causing their prices to decrease — deflation.

Generally, credit risk increases interest rates more for longer term loans than for short-term loans. The spreads for the 1-month and 3-month LIBOR-OIS rates have been reported by the press as representative of the credit risk in interbank lending.

The 1-month LIBOR-OIS spread has averaged 6 basis points from January, 2006 to August 1, 2007. During the Great Recession of 2007 and 2008, the maximum spread was over 100 basis points.

https://www.bloomberg.com/apps/cbuilder?ticker1=USSOA%3AIND

Screen clipping taken: 11/30/2008

Bloomberg.com: Investment Tools

https://www.bloomberg.com/apps/cbuilder?ticker1=USSOA%3AIND

Screen clipping taken: 3/20/2009, 12:02 AM