Financial Futures

The underlying assets for financial futures are foreign currency, stock indexes, and interest rates. Specialized futures were also recently introduced for single stocks, narrow-based indexes, and exchange traded funds. Financial futures expire every quarter in March, June, September, and December, partly explaining the so-called triple witching day that occurs on the 3rd Friday of these months, when options, index options, and futures contracts all expire, leading to increased buying and selling, and, thus, increased volatility on that day. Previously, these securities expired in the same hour — that is why it was called the triple witching hour — but the rules were changed so that expirations occurred throughout the day to lessen volatility.

Foreign Exchange Futures

Foreign exchange futures is part of the forex market that also consists of foreign currency, options of currency futures, and forward exchange transactions. The forex market operates 24 hours per day, 5 days per week.

A foreign exchange market exists because people, businesses, countries, and other organizations want or need currency of a particular country in order to buy products or services from that country or to receive aid or investment from foreigners. For instance, the European economy is now largely based on the Euro, so if an American travels to Europe, he will need Euros to pay for goods and services there. Thus, he will need to convert the U.S. dollars that he received at home to Euros to spend in Europe.

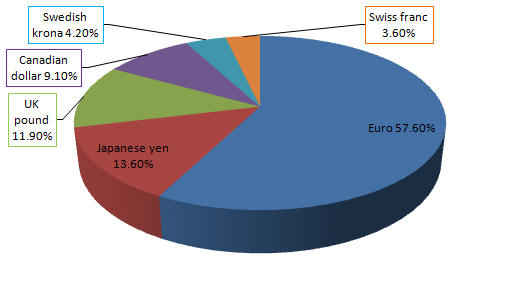

There are unique 3-letter currency symbols for each currency. Symbols for the most commonly traded currencies (also known as the major currencies) are:

| USD | United States dollar |

| CAD | Canadian dollar |

| AUD | Australian dollar |

| EUR | Euro |

| GBP | British pound |

| CHF | Swiss franc |

| JPY | Japanese yen |

The Bretton Woods agreement, in force 1944 - 1971 — created a fixed exchange rate among members by pegging currencies to the U.S. dollar, which was pegged at $35 per ounce of gold. The ratio of one currency to another was known as the par value of currency (or par exchange rate).

Since 1971, the world has used a floating exchange rate (or flexible exchange rate), where the value of any currency in relation to another is determined by the supply and demand of the respective currencies, which is determined by a country's reserve of gold, international trade balance, rate of inflation, interest rates, and the health of its economy and currency. In addition, a country may try to peg its currency to a specific exchange rate by buying and selling its own currency, as China does with the U.S. dollar. Currencies may fluctuate as much as 20%, or more, per year.

The 1st foreign currency futures were traded in 1973 at the International Monetary Market in Chicago. In addition to currencies, futures are also traded for the U.S. Dollar Index (USDX), which weights each currency in proportion to the amount of trade of the corresponding country with the United States. The 6 currencies and their current trade weights are:

When the dollar declines in value against this average, the index rises, and vice versa. Hence, businesses doing international transactions can use futures to hedge exchange rate risk.

Foreign currency futures contracts are settled either by the physical delivery of the currency, or by marking to market of the futures account.

Dynamic hedging is hedging only when it is advantageous according to one's price forecast — in other words, it's trying to time the market with futures. Thus, a short hedge would buy back his position if he thought prices will rise in the immediate future, so that he can sell his short position later for a higher price, and the long hedge would, for similar reasons, and if she shared the same forecast of higher prices in the immediate future, would buy the long position before the rise, then sell it when, according to her forecast, the price has peaked. Of course, the main risk with trying to time the market is that forecasts are frequently wrong, and thus, may lead to that common tactic for losing money — buying high and selling low, though not necessarily in that order. Dynamic hedging should probably be called dynamic speculation, because the trader is really trying to profit from short-term trades. However, some traders who are very familiar with the market for a particular commodity may have a better than average ability to predict general price movements over the year for that commodity, and, thus, will take a little risk for a greater profit through dynamic hedging.

Stock Indexes

Useful Websites for Foreign Exchange

Current foreign exchange rates for the world's major currencies. Includes key cross rates, a currency converter, and news about the currency markets. Provides cross rates for the U.S. dollar (USD), the United Kingdom pound (GBP), the Euro (EUR), and the Japanese Yen (JPY). Also has basic, advanced, and interactive charts that display the exchange rates over time.

Preventing Fraud

Some investors are losing money by sending money to fraudulent companies promising them riches by trading currencies, or by offering employment to solicit others in the scam. These investors are most often contacted by phone in boiler room operations, or by targeting specific ethnic groups. The best way to prevent fraud is don't respond to telephone solicitations, or to friends, who may have been defrauded themselves. Seek out and research any companies yourself with the help of these resources:

- Commodity Futures Trading Commission (CFTC) registrations, NFA membership information, and futures-related regulatory and non-regulatory actions contributed by NFA, the CFTC and the U.S. futures exchanges can be found by calling the National Futures Association at (800) 676-4NFA or by using their Background Affiliation Status Information Center (BASIC).

- The CFTC warns consumers of sales solicitations appearing in the news media, promoting high-returns and low-risk by trading foreign currencies, or by promoting highly paid currency-trading employment opportunities. Details about these schemes can be found at the CFTC's enforcement site.

- Additional information can be found at www.naag.org, the Attorney General's consumer protection bureau, and at https://www.consumeraction.gov/caw_state_resources.shtml, which list resources provided by states.

Futures on stock indexes were introduced in February, 1982 for the Value Line Composite Index on the Kansas City Board of Trade. Shortly thereafter, other indexes served as the basis for futures contracts: the S&P 500, the NYSE Composite Index, the Nikkei 225, and the NASDAQ 100. All of the major index futures can be found at Stock Futures of Major World Indexes.

There are also mini-contracts, with smaller multipliers, that correspond to some of the more popular indexes. In fact, one of these is the E-mini S&P 500 Futures, which is the most actively traded stock index futures contract.

The prices of stock index futures are calculated by multiplying the contract price by a specified number. For instance, the trading unit — the smallest size that can be bought or sold — for the CME S&P 500 Futures is $250 times the index price, whereas the multiplier for the E-mini S&P Futures contract is $50.

Because most indexes are a composite measure of a large number of stocks, hedging with stock index futures is most effective for large portfolios that closely mirror the index. The smaller the portfolio, the less effective the hedge will probably be, because individual stocks can move counter to the market, as they often do. However, even for large portfolios, stock index futures will rarely, if ever, be perfect hedges.

To make a more effective hedge, an investor or portfolio manager would divide the size of his portfolio by the contract size of the relevant futures.

Interest Rates

Interest rate futures were introduced by the Chicago Board of Trade (CBOT) in 1975. (CBOT is now CME Group. Here is a list of their Interest Rate Products.) There are futures on short and long-term interest rates, but the largest trading volume is in 2-year Treasury notes. The price of debt securities, and therefore interest rate futures, is inversely proportional to the prevailing interest rate. When the interest rate goes up, the price of debt securities and interest rate futures goes down, and vice versa. The yield settlement is the equivalent yield of the futures final settlement price.

Some of the assets underlying interest rate futures include U.S. Treasuries, Eurodollars, LIBOR, Swap, and Euroyen futures.

Treasury note futures are based on a standard issue with a fixed yield, but have a conversion factor that allows for the delivery of different securities with different yields to satisfy the contract, and the securities that can be delivered varies with the expiration month. For instance, CBOT uses a 6% interest rate for its Treasury futures, but few, if any Treasuries currently, have a 6% interest rate yield. The conversion factor normalizes the differences — if the interest rate is less than 6%, then the conversion factor is less than 1; if the interest rate exceeds 6%, then the conversion factor exceeds 1. The futures price equates to a cash price for a particular issue according to the formula:

Adjusted Futures Price (Cash Equivalent Price) = Futures Price × Conversion Factor

The seller determines what securities to deliver to satisfy the contract, which will be the cheapest for the seller to buy in the cash market. The futures price tracks this cheapest-to-deliver security (CTD) most closely.

Security Futures

Security futures includes single stock futures, narrow-based index futures, and exchange-traded fund futures (ETFF). Established by law for all security futures is an initial margin and maintenance margin requirement of 20%, although the customer's broker or futures commission merchant (FCM) may set a higher margin requirement. OneChicago is the main exchange for security futures, which are traded only electronically. The main benefits of security futures is that margin requirements are only 20% rather than the 50% required for the purchase or short-selling of stocks, and because there is no uptick rule for futures, they can be sold short at any time, without the need to borrow stock for shorting. Generally, security futures can be traded from either a brokerage account or a futures account.

There are typically 3 quarterly expiration dates, and 2 serial months, and these futures expire the 3rd Friday of the expiration month. Assuming no intervening holidays, physical delivery of stocks or futures is required by the 3rd business day after expiration, which is usually the Wednesday following the 3rd Friday.

Single Stock Futures (SSF)

Single stock futures (SSF) are futures for single stocks of mostly large companies, such as IBM, Intel, and Microsoft. As with all security futures, a margin of only 20% is required to take a position in an SSF, in contrast to the typical 50% of a stock purchase, and transaction costs may be less, especially for foreign stocks in countries with high transaction taxes and clearing charges.

An SSF contract calls for the delivery of 100 shares of the underlying stock on the expiration day; however, some SSFs may stipulate a cash settlement. Minimum price changes are a penny per share, or $1 per contract, with no daily price change limits.

Example: Leverage Increases Profits and Losses on Single Stock Futures

Suppose you purchase a futures contract for 100 shares of XYZ stock for $30 per share, or a total of $3,000 for the whole contract. If the margin requirement is only 20%, then you only have to put down $600 for the purchase. If, on the day of expiration, the stock price rises to $36 per share, then you've earned a total of $600 on an investment of $600 — a 100% increase. If you had used margin to buy the stock itself, then you would have had to deposit at least $1,500 to earn the same absolute return, but it would only be a return of 40%, and you would have had to pay interest on the remaining $1,500 that was borrowed to buy the stock. Because the margin in a futures account is really a performance bond, no money is actually borrowed, and, thus, no interest accrues. If you had paid for the stock entirely, then your rate of return would have been only 20% for a much larger investment.

On the other hand, if the stock had declined to $24, you would have lost 100% of your entire investment in the SSF, 40% of your margined stock investment, but only 20% if you owned the stock outright.

| Initial Investment | Stock Price Increases to $36 | Profit | Rate of Return | Stock Price Decreases to $24 | Loss | Rate of Return | |

|---|---|---|---|---|---|---|---|

| Buy Stock | $3,000.00 | $3,600.00 | $600.00 | 20% | 2400 | −600 | −20% |

| Buy Stock on Margin | $1,500.00 | $3,600.00 | $600.00 | 40% | 2400 | −600 | −40% |

| Buy SSF | $600.00 | $3,600.00 | $600.00 | 100% | 2400 | −600 | −100% |

The futures price of a single stock futures generally tracks the price of the stock, with differences due to the interest cost of carrying the stock, and the timing and amount of dividend payments.

Single stock futures prices generally conform to the following theoretical pricing formula:

Futures Price = Stock Price × (1 + Annual Interest Rate) − Present Value of Dividend Payments Prior to Expiration

The interest rate increases the futures price because the money that would otherwise be needed to purchase the stock can earn interest instead. Even the margin required for the SSF can be in the form of T-bills, or other interest-paying bonds or notes. The future value of all dividends paid before expiration decreases the SSF price because an SSF holder is not entitled to any dividends. Large dividend payments can actually lower the price of the SSF futures contract to less than the stock price.

Settlement may require the delivery of the stock certificates, or it may be cash settled. The owner of a single stock futures contract has no ownership interest in the company, has no voting rights, and receives no dividends.

SSFs provide an easier, and less risky, way than selling short to profit from stock price decreases. Selling a SSF does not require finding borrowed shares to short, nor can a futures contract be closed out involuntarily, as some shorted stocks can be in an illiquid market.

As with all futures contracts, traders sell futures because they expect the price of the underlying asset to decline, and traders buy futures because they expect the price to rise by expiration.

SSFs can be a good choice to profit from spreads.

Narrow Based Index Futures (NBIF)

These futures, cash settled, are for a narrow-based index of stocks, typically 3 to 7 stocks. They are provided for large institutional customers as OneChicago Select Indexes. In contrast to other security futures, the last day of trading is typically on the 3rd Thursday of the expiration month.