Mutual Funds

An investment in knowledge always pays the best interest.— Benjamin Franklin

A mutual fund company is an investment company that receives money from investors for the sole purpose to invest in stocks, bonds, and other securities for the benefit of the investors. A mutual fund is the portfolio of stocks, bonds, or other securities that generate profits for the investor, or shareholder of the mutual fund. A mutual fund allows an investor with less money to diversify his holdings for greater safety and to benefit from the expertise of professional fund managers. Mutual funds are safer, but less profitable, than stocks, and riskier, but more profitable than bonds or bank accounts, although its profit-risk profile varies widely, depending on the fund's investment objective.

It is easier to pick an investment strategy, such as growth or income, with mutual funds than by buying the individual securities, since mutual fund companies clearly specify the investment objectives of each fund that they manage. Other advantages to investing in mutual funds is that the initial investment is low, it is easy to reinvest profits, and money can be invested continually, such as every month, often in amounts less than the initial investment. It can even be done automatically.

Mutual Funds Versus Exchange-Traded Funds

Mutual funds and exchange-traded funds are similar, in that they both represent a basket of securities that lowers volatility and risk, but they have different advantages and disadvantages for investors.

- Mutual fund shares are purchased directly from the fund and sold to the fund only at the end of the trading day, which is the time when the price per share is set by the fund based on net asset value of the fund.

- No bid/ask spreads.

- Options are not available.

- Mutual funds may require an initial minimum investment, often ranging from $1,000 to $3,000.

- Mutual funds allow automatic investing by allowing the automatic periodic withdrawal of additional funds from checking or savings accounts.

- Taxable trades within the fund are passed to the investor, including capital gains.

Exchange-traded funds (ETFs) are investment companies that create and sell shares in a fund representing a beneficial interest in the holdings of the fund, which can include stocks, bonds, and other securities, and these ETF shares are traded on a stock exchange, and bought and sold through a broker-dealer, just like a stock.

- ETFs can be bought and sold from stock exchanges during market hours or even during extended hours.

- Trades allow stop or limit orders or selling short.

- Options are available.

- ETF prices may differ significantly from the underlying net asset values.

- Bid/ask spreads, wider for thinly traded ETFs

- There is no minimum deposit requirement, but they cannot be purchased by an automatic withdrawal of funds from checking or savings accounts.

- Fewer taxable trades within the fund are passed to the investor.

Mutual Fund Companies

Mutual fund companies are investment companies, registered under the Investment Company Act of 1940, that determine the investment objective of the fund, select the securities for the fund, operate the fund, and provide information and service to the investors.

Investment Adviser

Funds are managed by an investment advisor or by professional money managers under contract with the fund to invest to achieve the specific investment objectives of the fund, such as growth or income. The investment advisor, who could be officers of the fund or a management company, makes the daily investment decisions for the fund, and the fund's success depends on their ability.

The initial contract is for 2 years and must be approved by the board of directors and the shareholders. Afterwards, the contract must be renewed annually by the approval of the board of directors or the shareholders.

The prospectus lists the name of the investment adviser, their location, the term of their contract, and their principal duties and responsibilities. Their typical management fee is ½% of the fund's assets.

Board of Directors

Every investment company must have a board of directors, with no more than 60% of the board consisting of insiders, and at least 40% consisting of individuals who have no affiliation with the company, the fund's investment adviser, its underwriter, or any organization related to these entities.

Although the outside representation may be in the minority, several important decisions regarding the fund require the majority approval of the outsider representation to prevent conflicts of interest.

Custodian

A custodian, usually a bank, holds the money and securities in trust, and manages the relationships with the investors, such as sending the monthly financial statements and proxy forms for voting. It has no part in the investment choices or decisions of the fund.

Types of Investment Companies

The Investment Company Act of 1940 allowed the creation of 3 different types of investment companies:

- Face-Amount Certificate Companies

- Unit Investment Trusts

- Management Companies

- Open-end, which is the mutual fund.

- Closed-end

Face-amount certificates are rare. Think of them as certificates of deposits, where you pay a lump sum or pay in installments to face-amount certificate companies, who are the issuers of the certificates, in exchange for the face value of the certificate at maturity, or a surrender value if surrendered earlier. The difference between what you pay in and what you receive at maturity is the interest that you earned by purchasing the certificates. The face-amount certificate company earns money by investing the proceeds into other securities, much as a life insurance or management company does, which is why it is regulated under the Investment Company Act. However, unlike certificates of deposit, they are not FDIC insured, so it is possible to lose your entire investment. However, you may earn higher interest rates than would be possible to earn in a FDIC insured account. In fact, some companies that still issue them, such as Ameriprise Financial, also issue certificates whose return is linked to the stock market. If you are interested, you can get much more detail about how face-amount certificates work by reading this prospectus for Ameriprise Certificates.

Unit investment trusts are investment companies with trustees, but without a board of directors, that issue securities representing an undivided interest in the principal and income of a fixed portfolio of securities, usually consisting of bonds, but may also include mortgage-backed securities, or preferred or common stock. Unit investment trusts terminate either when the bonds mature or on a specified date. These securities trade just like stock or closed-end mutual funds. Many exchange-traded funds are organized as unit investment trusts.

Management Companies

The companies that operate mutual funds are called management companies in the Investment Company Act, and are classified as:

- open-end investment companies — commonly called mutual fund companies — which offers shares continuously and stands ready to redeem them,

- and the closed-end investment company, which makes a 1-time offering of shares, which are securities that can be traded like stock, but the company does not redeem the securities.

Open-End Mutual Funds

Most mutual funds are open-end funds, which sells new shares continuously or buys them back from the shareholder (redeems them), dealing directly with the investor (no-load funds) or through broker-dealers, who receive the sales load of a buy or sell order. The purchase price is the net asset value (NAV) at the end of the trading day, which is the total assets of the fund minus its liabilities divided by the number of shares outstanding for that day.

| Net Asset Value | = | Total Assets − Total Liabilities Number of Outstanding Shares |

The number of shares of an open-end fund varies throughout its existence, depending on how many shares are bought or redeemed by investors.

A major disadvantage to open-end funds is that they need cash to redeem their shares for investors who want out, so they either must keep lot of cash, which earns only the current prevailing interest rate, or they must sell securities to raise the cash, possibly generating capital gains taxes for the remaining investors of the fund.

Closed-End Mutual Funds

Closed-end mutual funds, also known simply as close-end funds (CEFs), sell their shares in an initial public offering (IPO), based on an advertised investment objective, such as for income or growth. The proceeds of the sale are then used to buy securities based on that investment objective. The CEF shares represent an interest in the portfolio of securities held by the closed-end investment company. The shares have a net asset value, just as open end mutual funds, but the closed-end investment company does not redeem the shares. Instead, the shares are traded on a stock exchange, just like stocks. Usually, when the shares are first offered, they are sold at a premium to their NAV. However, in the secondary market, the shares often sell at a discount to their NAV, because share price depends on the supply and demand of the market. Since there is no method available to exchange CEF shares for their underlying securities, arbitrage cannot be used to equalize the CEF share price to its NAV.

Exchange Traded Funds (ETF)

Closely related to mutual funds, and sometimes organized as unit investment trusts, exchange traded funds, sometimes called exchange listed portfolios, exchange index securities, exchange shares, or listed index securities, are like closed-end mutual funds in that they are based on a portfolio of securities representing a category or an index and are traded like stocks on organized stock exchanges.

ETFs differ from closed-end funds in that ETFs have an arbitrage mechanism that allows certain market makers or institutional investors, who have signed Participating Agreements with the fund sponsor, called Authorized Participants (also called creation unit holders), to exchange the basket of securities for creation units consisting of 50,000 ETF shares or a multiple thereof. The exchange involves only securities — no cash — which reduces capital gains taxes for shareholders. Only Authorized Participants can create and redeem ETF shares with the fund sponsor, and they also sell the ETF shares they create on the exchanges to retail investors.

When the ETF share price is significantly higher than the NAV, then Authorized Participants can buy the basket of securities on the open market, exchange the securities for ETF shares, then sell the shares on the market for a profit, which is how ETF shares are created. When the NAV is significantly higher, then the Authorized Participants trade their ETF shares for the basket of securities, then sell the securities on the exchanges for a profit, which is how ETF shares are destroyed. This process keeps the ETF share price and NAV approximately, but not exactly, equal, because it takes time and expense to profit from this difference through arbitrage, and the market supply and demand for both ETFs and their underlying securities, with the concomitant effect on prices, change constantly and quickly.

Like stocks and shares of closed-end mutual funds, but unlike open-end mutual funds, exchange-traded funds:

- can be bought anytime during market hours,

- can be ordered conditionally by setting limit orders,

- prices are based on market supply and demand for the shares rather than the underlying NAV,

- can be shorted even on a downtick,

- can be bought on margin,

- and options —calls and puts— can be based on them.

Expenses are very low, from .09% to .65%, because the securities that comprise the fund are not traded very often, and thus, do not generate capital gains tax liabilities for investors that results from such trades in a regular mutual fund or even a closed-end fund.

The first ETF, created by the American Stock Exchange in 1993, was the Standard & Poor's Depositary Receipts Trust, usually called a SPDR, or spider (ticker: SPY), and is based on the S&P 500 index. Two other major ETFs are the QQQQ (nickname: qubes) based on the NASDAQ 100, and the DIA (nickname: diamonds) based on the Dow Jones Industrial Average.

Mutual Funds Converting to ETFs

In 2019, new SEC rules governing investment funds allowed managers to more easily convert mutual funds to ETFs by eliminating the requirement for separate approval for each conversion, although conversions require shareholder approval.

Most of the conversions have been actively managed mutual funds, since they generate more fees than index funds. Actively managed ETFs have lower fees because they do not have to sell securities to pay for redemptions and they have tax advantages. ETFs also do not charge 12b-1 fees. However, ETFs do not offer fractional shares, so fractional shares of the former mutual fund are redeemed.

Investors who invested in the mutual fund through a transfer agent will need to have a brokerage account to receive and trade the new ETF shares.

Conversions to ETFs are also advantageous for the fund managers, since a converted ETF can keep both the performance record of the previous mutual fund and any investor assets that remain in the fund through the conversion, eliminating the need to market a new ETF.

Evaluating a Mutual Fund

When a mutual fund is created, the founders decide what market strategies to pursue and its investment objectives. A required prospectus is prepared for potential investors that details the company's objectives, expenses, fees, and management, so that an investor can make an informed decision about the mutual fund. When an investor buys the shares of the mutual fund, he becomes a shareholder of the company, with the same rights and privileges as a shareholder of any other company. For more info, read Mutual Fund Prospectus.

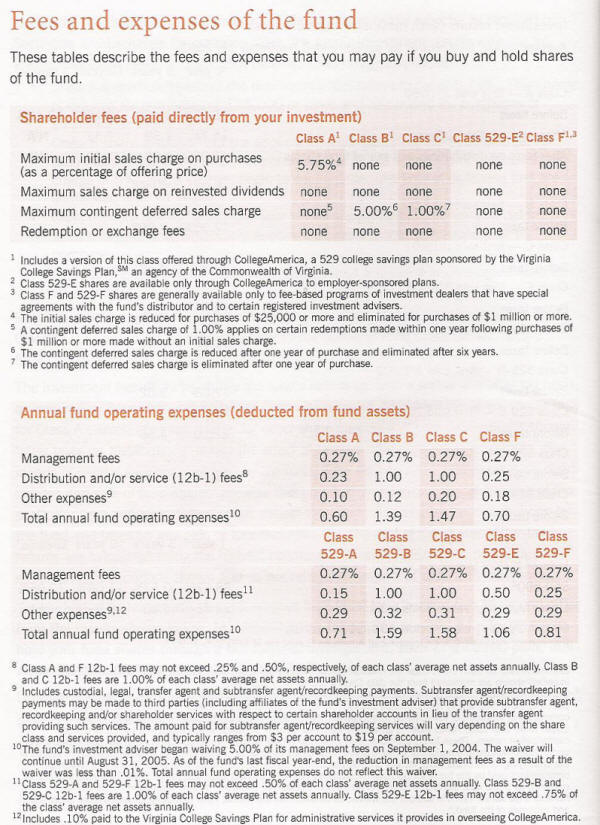

Fees

Many fees associated with specific activities may total from .5% to 8.5%, the legal maximum. Management fees are annual charges for administering the fund, which varies from about .5% to 2%. Distribution and service fees (12b-1 fees) cover marketing expenses to bring in new investors and may be used to pay bonuses for employees. Redemption fees, sometimes called a deferred sale load or back load fees, are assessed when shares of the fund are sold, to discourage frequent trading, unless the investor has held the shares for a minimum of time, specified in the prospectus. Reinvestment fees can be charged if the investor reinvests his profits in the fund. Exchange fees can be charged if an investor transfers his money from one fund to another within the same company.

No-Load Mutual Fund Fees

No-load funds do not charge a front-end sales charge or a deferred sales charge, such as a CDSC. FINRA rules also require that the 12b-1 fees not exceed 0.25% of the fund's average annual net assets to call itself a no-load fund.

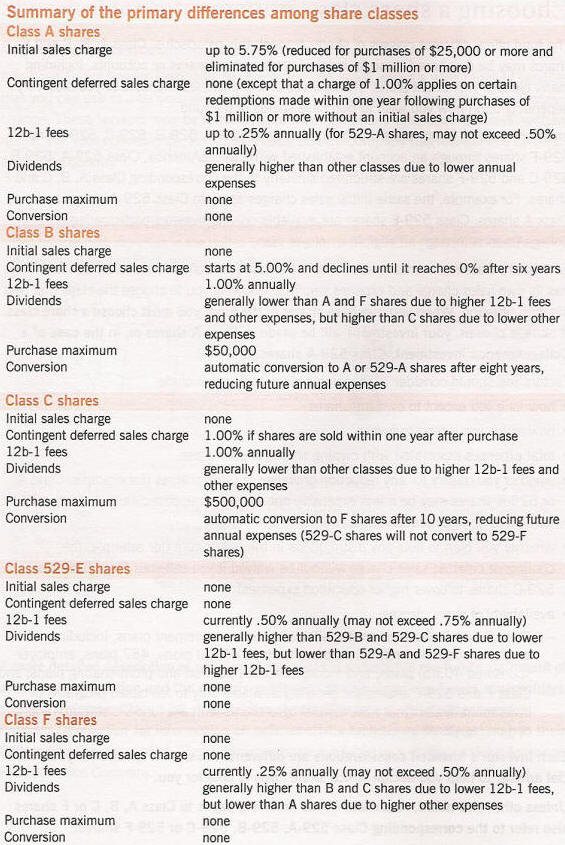

Classes of Mutual Fund Shares

Many mutual fund shares are classified according to the services provided the shareholders or distribution arrangements, with different fees and expenses and a different payment schedule that apply to each class. However, investment objectives and the portfolio secured of securities is the same for all classes, but because of the different expenses and when they are charged, there may be a slight difference in the performance of each class, depending on how long the fund is held and what class was purchased. This multi-class structure enables the investor to choose a class with fees and expenses that will yield the greatest benefit for the investor's expected holding time. More information about fees and expenses can be found in Mutual Fund Fees and Expenses. The following gives a sample of fees:

An example of share classes and the accompanying fees and expenses from an actual mutual fund prospectus:

Expense Ratio

Operating expenses, such as management fees, 12b-1 fees, and administrative fees, but not including transaction costs in the buying and selling of securities or fund shares (sales loads), can be summarized by the expense ratio:

| Expense Ratio = | Total Operating Expenses Average Net Asset Value |

The expense ratio is an important metric when comparing funds, because it can make a significant difference over time. Any money paid for expenses is money that is not invested and earns no profit. High expenses are not proportional to better management. In fact, frequently, high-expense funds underperform index funds, which are minimally managed and have very low expense ratios. A fund's managers can become rich simply by collecting expenses, even as the fund's NAV declines!

An example of a mutual fund fee table.

Investment Tips:

- Buy an index fund or an exchange-traded fund (ETF). Fund managers rarely do better consistently.

- Select an index fund or ETF with the lowest fees, since, if all other factors are equal, it will have the highest return among funds of the same index.

Measuring Mutual Fund Performance

A mutual fund can be measured in many ways: 3 common metrics are:

1. Net Asset Value (NAV) change. The NAV is the share price of the fund, obtained by dividing the value of the fund's holdings by the number of outstanding shares. The share price is what you must pay to buy into the mutual fund + any fees. The change in NAV, reported at the end of every market day, reflects the increase or decrease in the value per share.

| Net Asset Value (NAV) | = | Value of Fund Number of Shares |

| Net Asset Value (NAV) Example | |

|---|---|

| $100,000,000 total fund value 10,000,000 shares | = $10 per share |

2. Yield percentage is the amount of income from dividends and interest divided by the NAV, or price per share. A mutual fund yield can be easily compared to a bond yield.

| Yield % | = | Income Distribution per Share Price per Share |

| Mutual Fund Yield Example | |

|---|---|

| $.60 income per share $10 per share | = 6% yield |

3. Total return is the current value of shares + all distributions taken as cash minus the initial investment.

| Total Profit or Loss | = | Current Value of Shares + Cash Distributions − Initial Investment |

| Mutual Fund Total Return Example | ||

|---|---|---|

| $12,000 current value of shares + $3,000 total cash distributions − $6,000 initial investment | = | $9,000 Profit |

Investing in a Mutual Fund

Buying Mutual Fund Shares

An investor has a choice of buying shares of the mutual fund directly, or through a financial agent, such as a broker or a bank. Buying through an agent will cost more, and oftentimes, an agent will push funds that his company sponsors or earns the highest commission for the agent rather than what's best for the client. There are, however, good tools on the Web for finding funds that satisfy certain criteria.

Profiting from a Mutual Fund

A mutual fund earns money from dividends and interest, and by selling securities. Profits are paid to investors through distributions. Income distributions are based on profits from dividends and interest, while capital distributions are from profits from the sale of securities. The schedule of payouts differs according to company. Typically, income is distributed quarterly, while capital distributions are paid out once a year, usually in December.

Instead of receiving distributions, profits can be reinvested, but investors must pay tax on profits, whether it is distributed or reinvested. Income distributions are taxed as ordinary income, while capital distributions are taxed as capital gains.

An investor can also profit by selling shares back to the fund — redeeming the shares. Such sales are taxed as capital gains in the year they are sold. Depending on the mutual fund and the share class, there may be a deferred sales load on the redemption.

Regulation of Mutual Fund Companies

The Securities and Exchange Commission (SEC) monitors and regulates all mutual fund companies registered under the Investment Company Act of 1940. Mutual fund companies are also regulated by the Financial Industry Regulatory Authority (FINRA). Each state also has security regulations that may apply to mutual fund companies doing business in that state.

Most mutual funds are also regulated investment companies that comply with Sub-Chapter M of the Internal Revenue Code, which requires that the company must distribute at least 90% of its net investment income and 90% of its net capital gains to its shareholders to avoid corporate taxation of the distributions. Investment companies must, however, pay tax on undistributed income. If the investment company retains more of its income than is required to be distributed, then it is subject to a nondeductible 4% excise tax.

If a mutual fund is also a diversified management company, which most are, then at least 75% of its portfolio must consist of securities where no individual issue composes more than 5% of the fund's total assets, and that does not compose more than 10% of the voting stock of any single issuer. The other 25% of the fund is not so restricted.

What to Consider When Buying Mutual Fund Shares

Before buying many shares from a fund with a front-end sales load, check for breakpoints that could lower the sales load percentage.

No-Load Funds may have Fees for Purchasing or Selling Shares

No-load funds do not charge a sales load, which is technically a sales commission to a broker for selling the shares, and therefore the no-load category may include fees that are not technically sales loads, such as purchase fees, redemption fees, exchange fees, and account fees. No-load funds will also have operating expenses.

Lower Fees and Expenses Increases Total Returns and Yields; Higher Expenses Lowers Returns

Slight differences in fees can translate into large differences in returns over time. For example, if you invested $10,000 in a fund that produced a 10% annual return before expenses and had annual operating expenses of 1.5%, then after 20 years your investment would be worth $49,725. But if the fund had expenses of only 0.5%, then you would end up with $60,858 — an 18% difference.

Closet Index Mutual Funds — Active Share Percentage of a Mutual Fund

WSJ.com - Professors Shine a Light Into 'Closet Indexes'

It seems that some mutual funds that are supposed to be actively managed, aren't, but the managers are getting paid fees as if they are. A closet indexer is a mutual fund "manager" who runs a fund that charges a high fee, supposedly for active management, but that really is mostly composed of funds in an index, and, thus, the fund, after subtracting fees and expenses, lags the index.

Antti Petajisto and Martijn Cremers from the Yale School of Management have quantified how much a mutual fund really mirrors an index by comparing the components of an index with the holdings of mutual funds, as reported to the Securities and Exchange Commission. The active share of the fund measures the overlap between an index and the fund's holdings. The more the fund differs from the index, the greater the active share. A closet index fund is defined as one where the active share is less than 60%— the smaller the percentage, the less actively managed it is.

It was found that funds with an active share exceeding 70% beat their benchmark index by 1.39%, but those funds that closely mirrored the funds returned 1.41% less because of high fees. It was also found that the bigger the fund became, the more it mirrored the index.

If a fund does not do better than an index, then it makes sense to buy an index fund with low expenses, such as the Vanguard funds.

How Buying and Selling by Mutual Funds Affects the Stock Market

How Fund Rankings Can Cause Stocks to Gyrate - New York Times

Fire sales and forced purchases — a new study shows how mutual funds cause booms and busts in stock prices. Consider this explanation for the Internet stock bubble: technology sector funds initially outperform the market, then they receive large new infusions of cash from investors, which the sector funds promptly invest in their sector, causing the price to rise even more, then initiating another round of fresh infusion of cash, which is again invested in the sector, until...BUST! Nothing keeps rising forever. The technology sector starts to underperform, people move their money out of the funds, forcing the funds to sell technology stocks to pay for redemptions, causing the funds to underperform even more, causing more people to redeem their shares, forcing the funds to sell even more shares to pay for redemptions. Bottom!

Seems like a reasonable explanation. Some investment tips are offered in how to take advantage of this phenomenon.

SSRN-Asset Fire Sales (and Purchases) in Equity Markets by Joshua Coval, Erik Stafford

The actual study — Asset Fire Sales and Purchases in Equity Markets — can be downloaded here.Mutual Fund Managers Investing in their Own Mutual Funds

WSJ.com - Another Way to Assess a Mutual Fund

Mutual fund companies are now required by the SEC to disclose how much of a stake, or the lack thereof, that fund managers have in their own funds. Unfortunately, the SEC only requires this information in the statement of additional information, which usually must be requested from the company or it can be found at https://www.sec.gov/edgar.shtml. Some fund companies are also providing this information in the fund's prospectus or on its website.

A study of 1,300 mutual funds based in the U.S. by the Georgia Institute of Technology and the London Business School found that funds in which the managers of the fund also invested in it appreciated an average of 8.7% in 2005, the year covered in the study, versus 6.2% appreciation for those funds where the managers had no money in their fund, which included more than half of all mutual funds in the study. It also found that fund performance increased .03% for every .01% increase in manager ownership, and that manager investments were highest for domestic stock funds and lowest for international bond funds, although this may just reflect the fact that interest rates were rising in 2005, which is usually not good for bond funds, since the price of bonds declines when interest rates rise.

Many fund companies are now stipulating that some of their managers' compensation must be invested in the funds they manage.