Futures Orders: Buying and Selling Futures Contracts on an Exchange

After opening a futures account, you can place orders with your futures commission merchant or broker to buy and sell futures. Any such order must specify:

- whether it is to buy or sell,

- the quantity,

- the delivery month along with the year if necessary,

- the underlying commodity,

- the exchange if the commodity is sold on more than 1 exchange,

- the type of order, such as a market order or a limit order, and any contingencies.

Either buying or selling a contract is either an opening or closing transaction, because, except in special cases, you cannot be both long and short in the same futures contract at the same exchange in the same account. Thus, it is possible to be long in Chicago wheat and short in Kansas city wheat, but it is not generally permissible to be long and short in Chicago wheat in the same futures account. For instance, if you first sell a contract, you open a position in that contract, being short. If you subsequently buy it back, then your broker will treat the purchase as a closing transaction. However, if you had bought the contract first, then you would be long in the contract, and your purchase would be considered an opening transaction. Thus, whether the purchase or sale of a futures contract is an opening or closing transaction depends on what contracts are already in the account. When the exchange receives your order, the floor trader doesn't know nor does he care whether it is an opening or closing transaction, but it matters for you since it will determine your position in the futures market.

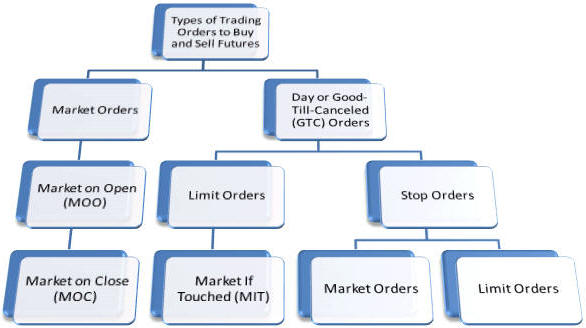

Market Orders

Unmatched orders in the trading system are limit orders. The limit order with the lowest sale price is the best ask price; the limit order with the highest buy price is the best bid price. A market order is an order, executed immediately, that will buy at the best ask price or sell at the best bid price. If limit orders are insufficient at the best bid/ask price to satisfy the market order, then the next best bid/ask prices will be used, etc., until the entire order is filled.

The risk with market orders is that the market price might be significantly different from the current quote in a thinly traded contract. Limit orders prevent this risk.

A market-on-close order is a market order to be executed right before the close of the trading day. However, as a market order, the price may differ from the final settlement price for the day. A trader may enter this order, if the price is expected to be better at the end of the trading day.

A market-on-open order (MOO) is a market order to be executed right at the opening of trading, but, as a market order, the transacted price may differ from the opening price. Orders accumulate when the market is closed, so a trader expecting excess buy or sell orders will try to profit from that bias by entering a MOO order.

Contingent Orders

If the order is not a market order, then it is a contingent order, because it may not be executed unless certain conditions are satisfied. A contingent order may be a day order or a good-till-canceled order. A day order expires at the end of the trading session. A good-till-canceled order (GTC) remains in the trading system until canceled, or until the limit of time imposed by the exchange or broker.

Contingent orders cannot be placed on the last trading day of the futures contract.

Limit Orders

A limit order is an order to buy or sell at a specific price or better. A limit order to buy at a specified price is an order to buy at that price or lower. A limit order to sell at a specified price is an order to sell at that price, or higher. Though a limit order guarantees getting at least the limit price if executed, its main risk is that the order will never be executed, or it will only be partially executed, and the market can move further away from the limit price, decreasing the likelihood that it will ever be executed.

Market-If-Touched (MIT) Orders

A market-if-touched order (MIT) is a limit order that becomes a market order if the market price reaches the limit price. Then the order is executed completely; however, the price may be worse than the limit price, because there was not enough contracts at the specified price to fill all the orders at that price. Thus, the risk of an MIT order is that it may not be executed, if the market price never reaches the MIT price, and if it does, the price may be worse than the MIT price. However, it does have an advantage over a limit order in that it will be executed completely if the market does reach the MIT price, whereas a limit order may only be partially filled.

Stop Orders

Stop orders are used to limit losses. A stop order is a market order to buy above the current market price or to sell below the current market price, but only if the market reaches that price. It is like an MIT order except the specified price to buy is above the current market price rather than below it, or the price to sell is below the current market price rather than above it. The only purpose for a stop order is to limit losses. However, the price received may be worse than the stop price, because as a market order, the order may be filled at a worse price, and in thinly traded futures, it may be a lot worse.

A stop limit order is like the stop order, but it becomes a limit order when the specified price is reached rather than a market order. The main risk to this order is that it may not be filled, because the market may skip over the limit price or other orders had priority at that price, or it may only be partially filled. Thus, it is not an effective order for limiting losses. However, it does guarantee the limit price or better, if executed, in illiquid or volatile markets.