Stock Rights Offering

Stock rights (aka pre-emptive rights, subscription rights, oversubscription privilege) are rights given to existing stockholders to purchase new issues of the company stock before it is offered to the public, so that existing stockholders can maintain proportionate ownership of the company, if desired. Most states have laws giving shareholders pre-emptive rights, but the company may, depending on the law, pay stockholders a fee to waive their pre-emptive rights or the pre-emptive rights may exist only if so specified in the corporate charter. Pre-emptive rights were more prevalent in the past, but are rare today in the United States. However, pre-emptive rights are prevalent in Europe since European security laws typically require that the companies offer their shareholders the right of first refusal.

So if a corporation offers pre-emptive rights and wants to raise more money by issuing new shares from its authorized, but unissued shares, it will offer rights to existing shareholders so that they can maintain their proportionate ownership of the company. The company will provide existing stockholders with subscription rights (aka rights certificates), giving stockholders the right, but not the obligation, to buy the new shares at a specified price — the subscription price — which is usually lower than the market price. A benefit for the company of selling to existing shareholders is that marketing costs will be less than selling to the public.

The Role of Investment Banks in a Rights Offering

Sometimes, a company will manage its own offering as a self-run deal, but, usually, the rights offering is handled by investment bankers in a standby commitment, where the investment bank agrees to buy any shares not subscribed to by the holders of rights. Hence, there is risk for the investment bankers. Investment banks charge a fee both for their services and to cover their risk of having to buy unsold shares, especially if the stock price drops below the subscription price. To reduce this risk, originating investment banks spread their risk by using an underwriting syndicate and selling groups, who, for a part of the fee, guarantee the sale of the securities.

Prior to the Great Recession of 2008, the fee was about 1.9% of the offering for deals of $250 million or more for the originating bank, and syndicate members got 1%. However, during the Great Recession, fees increased to 3% for the originating bank and 2% for the syndicate members for the increased volatility of the stock market, increasing the likelihood that the stock price would drop below the subscription price during the rights offering (Source: JPMorgan Takes Lead in Busiest Year for Rights Offers (Update1) - Bloomberg.com).

Standby Commitment for a Rights Offering: Lay Off

When the investment bank has a standby commitment with its client, then the investment bank agrees to purchase any subsequent new issues of stock shares not purchased by current stockholders in a rights offering at the subscription price, which it will then sell to the public as a dealer in the stock.

Besides using an underwriting syndicate, another method to reduce the risk that the price of the stock could decline during the 2 to 6 weeks of a rights offering is to do a lay off, where the investment bankers:

- buy rights sold by the current stockholders, then exercising the rights and selling the stock;

- or by selling enough stock short, up to 1/2% of a new issue, to cover an expected proportion of unexercised rights, then using the rights to cover the short.

Calculating the Value of a Rights Offering

A stockholder usually receives 1 right for each stock owned at the rights record date, when the rights certificates are issued to shareholders as of the rights record date. This gives the stockholder the right, but not the obligation, to buy additional shares of stock at the subscription price. To buy an additional share of stock requires a certain number of rights, and the number of rights required will be the quotient of the number of issued shares divided by the number of newly issued shares. If there is a remainder, then there will be a dollar amount added to the number of rights required to purchase each share. This will allow the shareholder to buy enough shares to maintain proportionate ownership, but no more.

| 1 Share of Stock | = | Issued Shares Number Newly Issued Shares Number | Rights | + | Possible Specific Dollar Amount |

Thus, from the above formula, if no additional money is required, the number of rights that must be exercised to receive 1 share of stock is:

| Number of Rights Needed for 1 Share of Stock | = | Issued Shares Number Newly Issued Shares Number |

Example: How a Rights Offering Can Preserve the Proportional Ownership of Its Current Stockholders

- A company has 10 million shares of stock outstanding and wishes to issue 1 new million new shares, so it issues 1 million rights to its current stockholders so that they can maintain their proportionate interest, if they desire.

- You have 1000 shares of the company stock, so you receive 1000 rights.

- The number of rights needed to buy 1 share of stock = 10,000,000/1,000,000 = 10, so you exchange your rights for 1000/10 = 100 shares of stock.

- Before the rights offering, you owned 1000/10,000,000 = .01% of the company.

- After exchanging your rights for the stock, you now have 1100 shares of stock, which represents 1100/11,000,000 = .01% ownership of the company, thus preserving your ownership percentage.

When a stock with rights is trading on the stock exchange, it is said to have cum-rights, and it will have a higher market value than the same stock trading ex-rights (aka rights off) — without rights. The ex-rights date begins 2 days before the rights record date and ends when the rights expire. From the time of the announcement of the rights offering to the ex-rights date, the rights are attached to the stock. During the ex-rights period, the rights are sold separately, just like a stock.

| Value of 1 Cum Right | = | (Stock Market Value − Subscription Value) (Number of Rights needed to Buy 1 Share of Stock + 1) |

However, this value is theoretical because the right is attached to the stock, so it is bought and sold with the stock during the cum-rights period. During the ex-rights period, the rights are sold separately, like a stock, and the formula is the same, but without the +1 in the denominator.

| Value of 1 Right | = | (Stock Market Value − Subscription Value) Number of Rights needed to Buy 1 Share of Stock |

When the rights expire, usually 4 to 6 weeks after the ex-rights date, they become worthless.

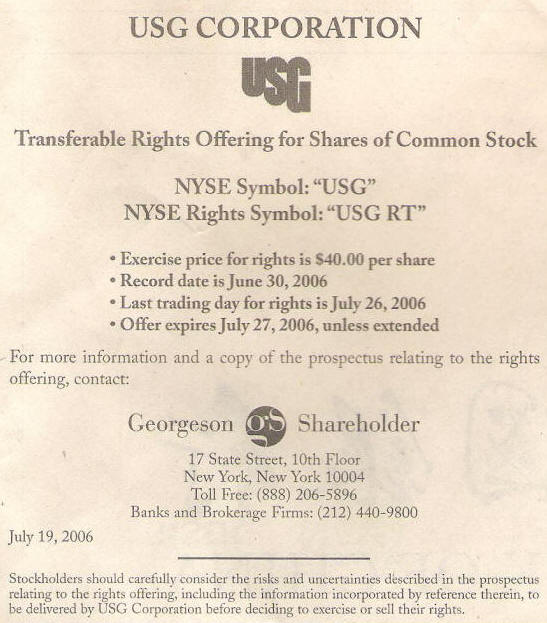

Real-World Examples of Rights Offerings

Though these examples are more than 10 years old, they still illustrate rights offerings.

Real World Example of a Rights Offering

The illustrated timeline below shows the events of a stock rights offering by Milacron.

Bonus Issues (aka Capitalization Issues, Scrip Issues)

Sometimes, a company wants to move money from a reserve account to a capital account on its balance sheets to convert reserve capital into ordinary share capital. To accomplish this, the company will issue more shares for this extra cash in the capital account as bonus issues to current shareholders in proportion to their holdings, which is like a rights offering, but the current shareholders need not pay for the new issue. However, the company does need the approval of the shareholders to issue bonus shares.