Investment Banking: Issuing and Selling New Securities

When a company or other organization wants to raise funds, it frequently does so by issuing and selling new securities, such as stocks or bonds. Investment banks help in this process by providing expertise and customers to buy the securities. A company does not need to use an investment bank, but it usually does, because it is less costly than trying to issue and sell securities directly to the public.

An investment bank is not a bank in the usual sense. It doesn't offer checking or savings accounts, nor does it make auto or home loans. It is a bank in the general sense, in that it helps businesses, governments, and agencies to get financing from investors in a similar way that regular banks help these organizations get financing by lending money that the banks' customers have deposited in the banks' savings, checking, and money market accounts, and CDs. In other words, investment banks act as financial intermediaries for businesses and other large organizations, connecting the need for money with the source of money.

An investment bank helps an organization, which may be a company, or a government or one of its agencies, in the issuance and sale of new securities. It is usually a division of a brokerage because many of their activities are related. New issues include all initial public offerings (IPOs) of equities sold under a registration statement or offering circular. When a new issue is sold, any subsequent sales of the stock are called the aftermarket for the new issue.

To prevent unfair advantages to insiders, the Financial Industry Regulation Authority (FINRA), which promulgates many of the rules and regulations for securities industries operating within the United States, prohibits member firms or any persons associated with them from offering or selling the new issue to any account in which a restricted person has a beneficial interest unless an exception applies. Restricted persons include FINRA member firms and any associated people and immediate family members of the employee, including spouse, children, parents, siblings, in-laws, and any person who is a dependent of the employee. This restriction only applies to immediate family members buying an issue from the person employed by the member firm. Also restricted are portfolio managers, or anyone materially supported by them, who would be in a position to direct future business to the firm.

When an organization needs funds, it will first discuss the options and possibilities with an investment banker:

- how much money will be needed,

- what type of security to sell and any special features it might have,

- at what price, and

- at what cost to the company.

Today's investment banks generally provide other services, such as risk management, asset management, mergers and acquisitions, clearing and settlement, and even act as a principal rather than as an agent in transactions, although the other services may involve the issuance of securities. For instance, risk management is generally effected through the sale or purchase of derivatives. Thus, many investment banks today are not simply investment banks, but nonetheless, this article will examine investment banking as a pure concept, not as an actual embodiment of the investment banks of today, such as Goldman Sachs.

Underwriting Agreement, Firm Commitment

If the investment bank and company reach an agreement to do an underwriting — aka firm commitment — then the investment bank will buy the new securities for an agreed price, and resell the securities to the public at a markup, bearing all the expenses associated with the sale. The company gets the guaranteed funds even if the investment bank does not sell all the securities. Thus, the investment bank takes significant risk in a firm commitment. Often, the investment bank becomes a broker-dealer, or market-maker, in the new security.

Direct responsibilities in an underwriting include:

- registering the new securities with the Securities and Exchange Commission,

- setting the offering price,

- possibly forming and managing a syndicate to help sell the new securities, and

- to peg the price of the new issue by buying in the open market, if necessary.

Selecting the Right Offer Price is very Important in an Underwriting

If the offer price is too high, the investment bank will fail to sell all the new issue (aka undersubscription), then it must hold some of the issue in inventory, hoping to sell it later. If the investment bank holds the new issue in inventory, this will tie up capital that can be used elsewhere, or, worse yet, it may have to borrow money. Furthermore, the initial customers who paid a higher price for the new issue will be disappointed that they paid a higher price, and the investment bank may lose these customers in a future offering. The bank may also submit a stabilizing bid until either the new issue sells out, or it ends the offering and just takes the loss.

If the offering price is too low, then the new issue will quickly sell out, and the price of the new issue will rise quickly because the supply will be limited (aka oversubscription), inducing the initial investors to sell for quick profits — commonly called flipping. However, the company will not reap any of this extra money, and it will be disappointed that the initial offering price was not higher. Investment banking is a very competitive business. The issuer and other companies will see this as a failure to set the best price, and may take its future business elsewhere.

Selling a Hot IPO through a Dutch Auction

In a hot IPO, when many investors are clamoring to get shares, many of those who do get the newly issued shares will flip it — immediately sell it in the open market for instant profits. The investment bank must, by law, sell the new shares at the offering price regardless of demand. With higher demand for the new issues, they must be allocated, and usually it's the biggest clients of the investment bankers who get the issue — small investors almost never participate. Furthermore, neither the investment bankers nor the issuer can profit from flipping. However, flipping indicates that the offering price was set too low, but, on the other hand, the bankers don't want to set the price too high so that they can be sure to sell the entire issue quickly.

With a hot IPO, it is difficult to ascertain what price would be best, so some companies use a Dutch auction to determine the price. Google used this method for its IPO, for instance. In a Dutch auction, the public is invited to submit closed bids, indicating how many shares they want and at what price they are willing to pay. Then the company sets the offering price that will sell out the whole issue. Everyone who bid at or above the offering price will get shares at the offering price, even if they bid higher. Those who bid below the price will get no shares. The successful bidders may not get all the shares they requested, because there will not be enough, so the shares will be allocated proportionally to the amount requested divided by the total amount requested by all bidders. So, if the successful bidders requested 10,000,000 shares, but there are only 2,000,000 shares available, then each bidder will get 20% of whatever they requested.

Standby Commitment for a Rights Offering, Lay Off

When the investment bank also has a standby commitment with its client, the investment bank agrees to purchase any subsequent new issues of stock shares at the subscription price that are not purchased by current stockholders in a rights offering, which it will then sell to the public as a dealer in the stock.

The investment bank takes a risk, however, in that the price of the stock could decline during the 2 to 4 weeks of a rights offering. To minimize this risk, the investment bank may do a lay off:

- buying up any rights sold by the current stockholders, then exercising those rights and selling the stock;

- and by selling enough stock short, up to 1/2% of a new issue, to cover an expected proportion of unexercised rights, then using the rights to cover the short.

Best Efforts Underwriting

Most agreements for the sale of new securities are an underwriting, but sometimes the investment bank will agree to a best efforts approach because the company is perceived as a risky investment for a new issue. The investment bank will do its best to sell all the new securities, but it does not guarantee it. The company bears the risk that the investment bank may fail to sell all the new issue, thereby lessening the amount the company receives.

Best-efforts underwriting have 2 variations: all-or-none or mini-max. An all-or-none underwriting requires that the entire issue be sold within a specified time, or else the program is terminated. A mini-max underwriting (aka part-or-none underwriting) is similar, except that only a specified minimum must be sold. In either case, SEC Rule 15c2-4 requires that all money collected from any sales be deposited in a separate escrow account at an independent bank for the benefit of the investors. If the sale is canceled, then the money must be returned to the investors, and no more orders will be taken; if the underwriting is successful, then most of the money goes to the issuer minus the fees paid to the underwriters.

Underwriter Compensation

The underwriters make their money by selling the new securities at a markup from what they paid for it, called the underwriting discount or underwriting spread. The underwriting discount is set by bidding and negotiation, but is influenced by the size of the new issue, whether it is stocks or bonds, and the perceived difficulty of selling the new issue, with more speculative issues requiring a larger underwriting spread for the increased risk. The flotation costs of the new issues, the total cost of bringing the new securities to market, also includes legal, accounting, and other expenses borne by the issuer in addition to the underwriting discount. Flotation costs are generally a greater percentage of the total sale of the new securities for small issues than for larger issues, greater for stocks than for bonds. The underwriting spread may vary from about 1% for investment-grade bonds to almost 25% for stocks of a small company.

As additional compensation, the underwriting firm may also get rights to buy additional securities at a specified price, or receive a membership on the board of directors of the issuing company. The underwriting firm frequently becomes a market maker in the new security, keeping an inventory and providing a firm bid and offer price for the new security to provide a secondary market so that investors can buy or sell the new securities after the primary sale. Providing liquidity for investors increases the value of the primary offering since few investors would buy the new security if they couldn't sell it at will.

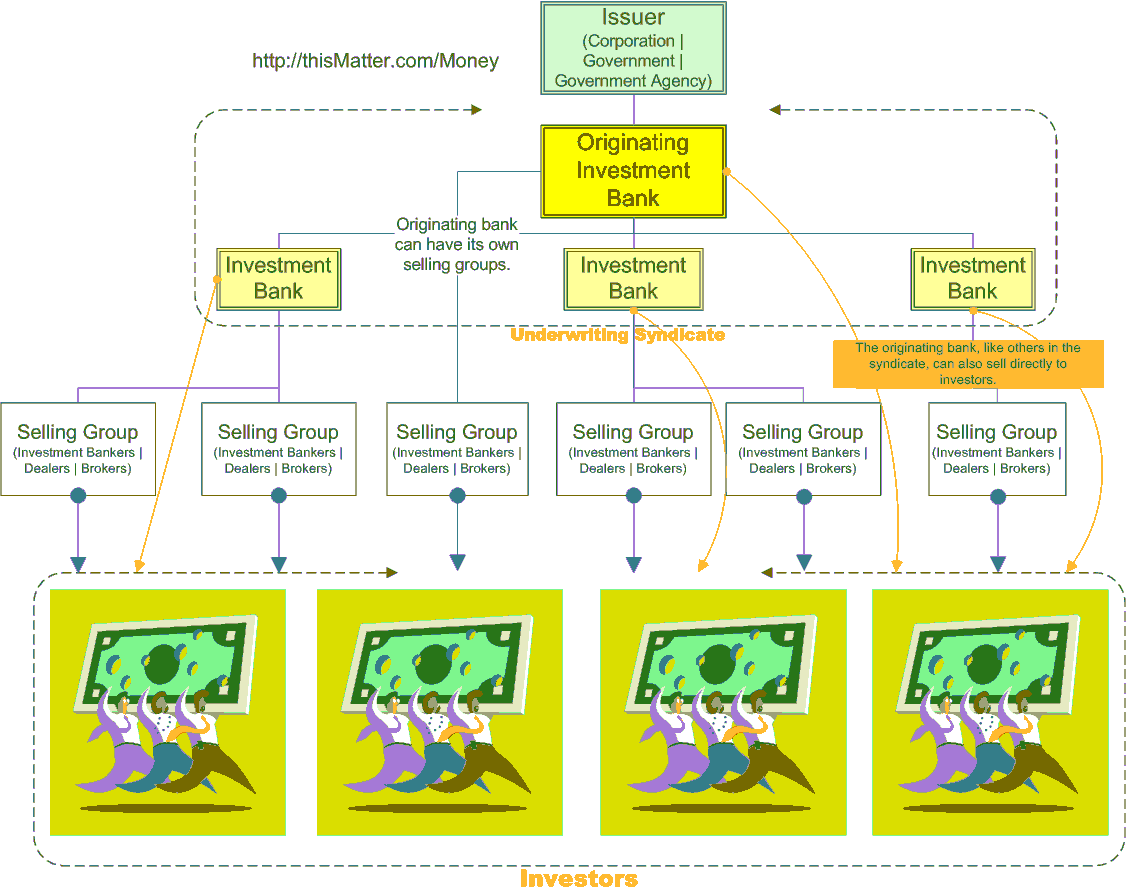

Syndication: Enlisting Other Investment Banks to Sell the New Securities

Sometimes the investment bank will enlist the help of other investment banks to sell the securities, forming a underwriting syndicate. The investment bank, which could be multiple firms that the company selected, is called the originating house (aka syndicate manager, managing underwriter), which selects the members of the syndicate and determines how many shares each will get, and manages the overall process. The underwriting manager determines, along with the issuer, the offering price and the time of the offering, and controls all advertising for the new issue. The managing underwriter not only handles the federal registration, and responds to any deficiency letters from the SEC, but since state security laws (aka Blue Sky laws) require that the new issue must be registered in each state in which it is offered, the manager also ensures that the security has been Blue Skyed.

The members sign an Agreement Among Underwriters (AAU), stipulating, among other things, the management fee, and that they will represent the issuer. Also stipulated is the percentage of each underwriter's allotment of the new issue. There may be an overallotment provision (aka green shoe, because this provision was 1st used in an underwriting for the Green Shoe Company ) that will allow the underwriters to get more shares at the original price if the issue turns out to be oversubscribed.

Each member of the syndicate must also sign an Underwriting Agreement (UA) stipulating the relationship between syndicate members and the issuer, including their rights, obligations, terms, and conditions, and that the issuer is required to sell and the syndicate members must purchase a specified number of shares. This agreement is signed when the registration of the new securities becomes effective.

There are 2 types of obligations concerning the purchase of the new issue by the syndicate members. The most common type — the divided account, or Western account — requires that the syndicate member sells its allotted shares of the new issue, but it is not obligated to sell the unsold shares of other members. The undivided account (aka Eastern account) requires each underwriting member to buy not only his own allotted shares, but also the same percentage of unsold shares of other members as the member's allotment percentage.

Example: Western and Eastern Accounts

5 members of the syndicate are each allotted 20% of a new issue of $100,000,000 of securities. All but $5,000,000 has been sold. If the members are bound by an Eastern account, then each member will be required to buy 20%, or $1,000,000, of the unsold shares. If, however, they agreed to a Western account, then no member must buy the unsold shares of any other member.

In addition, each member of the syndicate, including the originating investment bank may have selling groups (also called selling syndicate), consisting of other investment bankers, dealers, and brokers, that may also sell to investors. Members of the selling group, which can number in the hundreds for some issues, sign a Dealer Agreement (aka Selling Agreement) stipulating the terms of the relationship, including the commission (also called the selling concession), the date of termination — typically 30 days — and whether the selling groups have to buy unsold shares.

The main advantage of syndication is that it reduces risk by sharing it among the syndicate members, and each syndicate member and their selling groups have their own customers to whom they can sell the new issues, so it reduces the amount that any one brokerage must sell, making it more likely all the new issue would be sold.

A typical compensation arrangement for a syndicate is the originating house gets a small percentage of the underwriting spread of the entire issue; the other members of the syndicate get a percentage of all issues sold by them or their selling groups; and the selling groups get a percentage of what they sell. Below is a typical compensation schedule for a new security priced at $20 per share:

| Public Offering Price | $20.00 | per share |

| Manager's Fee | $.25 | The underwriting manager receives this for all share's sold. |

| Underwriter's Allowance | $1.75 | The syndicate member receives this for every share that it sells, either by itself or through its selling groups. |

| Selling Concession | $1.00 | What the selling group earns per share, which is paid out of the underwriter allowance. |

| Reallowance | $.50 | Per share for a broker or dealer who is not part of the syndicate or any selling group, which is paid out of the underwriter spread. |

| Amount Received by Issuer | $18.00 | per share |

Note that the underwriting manager and other members of the syndicate can also sell directly to investors, and if they do, they get the percentage that would otherwise go to compensate everyone below them. So if the underwriting manager sold directly to their institutional investors, for instance, then the manager would get the full $2 of the underwriting spread. If a member of the syndicate sells to their own customers, they would get $1.75 of the spread, because $.25 of that spread still goes to the underwriting manager.

The underwriters may attempt to stabilize the new issue, if it sells significantly below the IPO price. Stabilization is when the managing underwriter bids for the securities in the open market at or near the public offering price to maintain its price until all the issue has been sold.

Many Companies List Their IPOs on Foreign Stock Exchanges

Many United States companies list their IPOs on foreign exchanges, especially Australia, Britain, Canada, Hong Kong, South Korea, and Taiwan. The most common reason for going offshore include lower underwriting, legal, and other administrative costs and greater visibility in markets where greater growth is expected. For instance, a company can list an initial public offering on the Alternative Investment Market (AIM) for 10% to 12% of raised capital compared to 13% to 15% on NASDAQ.

Another good reason for listing on foreign exchanges is to have greater visibility where more growth is expected. Integrated Memory Logic, for instance, not only has its largest customers in Asia, but its largest suppliers are also located there, so it made sense for the company to list in Taiwan. Samsonite, an American company since 1910, had a $1.5 billion offering in Hong Kong, because it is central to where it expects most of its growth.

Investment banks in the United States prefer larger deals — typically, $500 million or more — not only because banks earn larger fees, but also because the deal is easier to sell to larger institutional investors who prefer stocks with larger floats, so that their large purchases or sales of the stock will affect the stock price less, lowering their liquidity costs.

Another factor is the lower costs of maintaining a listing. In the United States, the cost typically ranges from $2 million-$3 million annually, especially since the enactment of the Sarbanes-Oxley rules, depending on the size of the company, compared to $320,000 on AIM or $100,000-$300,000 in Taiwan.

A major drawback for United States companies listed on foreign exchanges is that travel time and other costs associated with conducting a road show to increase interest in the stock among the local population will be higher.

Private Investment in Public Equity Securities (PIPES)

Private investment in public equity securities (PIPES) are unregistered securities, which can be stock or convertible debt, issued by small-cap, high growth companies that are sold in a private placement to institutional investors at a 5% - 15% discount to the issuer's common stock. The company then tries to register the PIPES with the SEC so that they can be sold to the public by the original investors. PIPES allow a small company — which cannot get loans or more traditional financing because the company is too small, unproven, or too heavily in debt — to avoid the time and expense of a public offering, and receives immediate cash.

PIPES have surged recently, but the SEC has significantly slowed the registration of these securities for the risks, which include insider trading and the significant dilution of the common stock, which can lower stock prices. Often, the number of shares issued as PIPES is more than the number outstanding, so the SEC has been reluctant to register more shares than 33% of the public float — the number of shares held by the public, to prevent significant dilution and the consequent undermining of the common stock price.

Alternative Investment Market (AIM) of the London Stock Exchange

AIM (Alternative Investment Market), launched in 1995, is part of the London Stock Exchange for new companies, that requires less money and less disclosure to get listed than it does on an American exchange, leading to more new companies being listed than for the New York Stock Exchange and NASDAQ combined. Half of AIM's 1600 companies have listed since 2005, with almost 300 companies outside of the U.K. 90% of the companies have market values of less than £100 million (about $197 million).

To get listed on the London Stock Exchange, the Financial Services Agency of Britain reviews listings to prevent fraud, much as the SEC reviews listings for new companies before they can offer shares to the American public. AIM uses nomads, instead.

Nominated advisers, or nomads, who typically work for a stockbrokerage, reviews the company's documents to learn about management, financial controls, and growth potential, to decide if it should be listed on AIM. If approved, then companies must pay an annual fee of $7,595 to the exchange, and $40,000 to $100,000 to their nomad. To contrast, the annual cost of an NYSE listing ranges from $38,000 to $500,000, and NASDAQ, $21,225 to $75,000.

Once listed, the nomad provides advice on handling news and is supposed it ensure that the company is serving shareholders well. Because many nomads tout the companies under their watch, they have a vested interest in presenting the company in the best possible light, making any information they provide about the company suspect. The London Stock Exchange has 14 people monitoring nomads and any unusual price movements in any stocks. An external committee handles any discipline deemed necessary. If a nomad, who cannot sanction the company for violations, has any qualms about its company, the nomad is required to contact the London Stock Exchange.

There are a few conflicts of interest in using nomads as overseers. If a nomad resigns, for instance, trading of the company stock is halted until a new nomad is found. Another conflict of interest arises because the listed company can dismiss its nomad, whose brokerage would lose the fees paid for nomads, which could cause nomads to overlook irregularities.

Companies listed on AIM have not generally done well. The FTSE AIM Index is down slightly, compared to the 16% growth in the Russell 2000 Index, which is composed of companies similar in size, for the same period.

Pink Sheets, LLC, is planning a similar service in the United States, referring to the nomads as the Designated Adviser for Disclosure, or DAD.

Investment Banks Investing in Businesses rather than Managing the Initial Public Offering

Many investment banks, either with their private equity divisions or by using the firm's own capital, are investing in Asia by investing in the companies rather than managing their initial public offerings. The profits of selling its stake in the IPO can easily exceed what can be earned in investment banking fees. Moreover, such private equity investments foster relationships with the companies and provide investment banks with many advantages in the foreign country, such as providing new clients for its investment banking business.

For instance, Goldman Sachs Group, Inc. invested $2.58 billion of its own capital for a 5.75% stake in Industrial & Commercial Bank of China (ICBC). In 1994, Goldman and Morgan Stanley each invested $35 million in Ping An Insurance (Group) Co. Later, the 2 rivals sold their combined 9.91% stake for $1 billion.