Taxation of Mutual Funds

The taxation of mutual funds is more complex than for stocks, because a mutual fund is a pass-through entity — the mutual fund does not pay taxes on its transactions; instead, the tax consequences of the transactions are passed through to the investors. The investor will typically receive the following types of distribution: ordinary and qualified dividends, tax-exempt interest and dividends, capital gain distributions, and return of capital distributions. Thus, the investor will realize a gain or loss from these distributions, but the different types of distributions are subject to different tax rules.

The source of mutual fund taxable dividends is either from stock dividends held by the fund or from short-term capital gains. A return of capital distribution is not taxable, since it is considered a return of the taxpayer's investment. However, the taxpayer's basis must exceed 0; if it is less, then any return of capital exceeding the basis is taxable, since it is income.

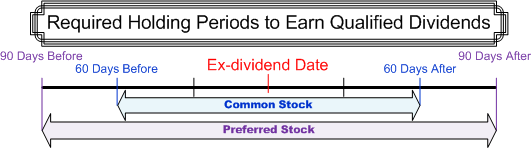

Starting in 2012, mutual funds may also distribute qualified dividends, which are taxed at the long-term capital gain rate, which is 0% for those in the 12% tax bracket or less, and 15% for those in higher brackets but who do not have to pay the new 3.8% Medicare surtax; otherwise, the rate will be 18.8%. The rate for taxpayers in the top bracket is 23.8%, since they are subject to a 20% long-term capital gains rate rather than 15%. However, for the mutual fund investor to benefit from qualified dividends, both the mutual fund and the taxpayer must satisfy the holding periods for the qualified stock.

How the Time of Investments Affects Taxes

When a mutual fund is about to make a capital gains distribution, the share price is higher to reflect the imminent distribution of that income. If a taxpayer buys the fund right before the ex-dividend date, then she will receive a portion of the capital gains distribution proportional to her investment in the fund, but she must pay taxes on that distribution.

If the taxpayer wishes to avoid paying taxes on the distribution so soon after buying the mutual fund shares, then the timing of the distribution can be checked on the fund's website or the taxpayer can call the fund to find out when the fund will be paying distributions.

Most mutual funds declare yearend dividends, generally in October, November, or December. Even if the dividend is paid in the following year, the distribution is taxable in the year that it was declared.

Reinvestments: dividends and capital gains distributions can be automatically reinvested by the fund, if the investor so desires. Dividends and distributions are reported on Form 1099-DIV, Dividends and Distributions. Whether dividends and distributions are received in cash or reinvested, they must be reported as income. If the taxpayer redeems fund shares at a loss within 30 days either before or after a distribution, then a wash sale may result, in which case, the loss cannot be deducted, but must be added to the cost basis of the mutual fund shares.

If a mutual fund holds tax-exempt bonds, then the interest earned from them is tax-free. However, any capital gain distributions resulting from the sale of those bonds are taxable — only the interest is tax-free. However, if any of the exempt interest dividends come from private activity bonds, then the interest will be a preference item in determining the alternative minimum tax (AMT). If tax-free interest is received on shares held 6 months or less, which is subsequently sold at a loss, then the basis of the shares must be decreased by the amount of the exempt interest in calculating the loss (on Form 8949, Sales and Other Dispositions of Capital Assets). For instance, if the taxpayer's basis in a mutual fund is $50 per share, who then receives $5 per share as tax-exempt interest, then no loss can be claimed on the shares held 6 months or less unless the sale price is less than $45 per share.

Ordinarily, expenses are not considered income. However, for a nonpublicly offered fund, expenses are reported as a taxable dividend even though the shareholder did not receive the distribution. Previous to the 2017 Tax Cuts and Jobs Act (TCJA), these expenses were deductible but only as a miscellaneous itemized deduction, subject to the 2% AGI floor on Schedule A, but the TCJA eliminated this deduction.

Tax Credits for Mutual Funds

Sometimes a mutual fund will retain their long-term capital gains and pay tax on it. The taxpayer must still report the capital gains, while the payment is also reported on Form 2439, Notice of Shareholder of Undistributed Long-Term Capital Gains, which is sent to the taxpayer by the fund. The basis of the taxpayer's shares is increased by the amount of the undistributed capital gain that exceeds the tax paid on that gain. A mutual fund may also pay foreign taxes for the foreign securities that it holds, in which case, the shareholder could claim either the foreign tax credit or take a deduction. The mutual fund should provide instructions for claiming the credit or the deduction.

Redemptions and Exchanges

When an investor wants to exit an investment in a mutual fund, he sells the shares back to the mutual fund, and in the process, incurs a capital gain or loss. If the shares of one fund are exchanged for another, even within the same fund family, it is still treated as a sale. The gain on shares held for longer than 1 year is treated as a long-term capital gain or loss. If the shares were held for 6 months or less but the taxpayer received a capital gain distribution in the meantime, then any loss incurred in redeeming the shares must be divided into a short-term capital loss and a long-term capital loss, the long-term capital loss being equal to the amount of the capital gain distribution. So if an investor pays $1000 for the shares, receives a capital gain distribution of $100, then redeems the shares after 5 months of ownership, for $700, then the investor should report a long-term capital loss of $100 and a short-term capital loss of $200.

To determine gain or loss, the mutual fund shares have to be identified, if the number redeemed is less than the number bought. The holding period for the shares begins the day after the trade date — not the settlement date — and ends on the redemption date. Each new month of the holding period begins on the same day of the month, regardless of the number of days in the prior month.

The gain or loss on the redemption of mutual fund shares is determined on Form 8949, Sales and Other Dispositions of Capital Assets and Schedule D, Capital Gains and Losses.

Cost Basis Methods: Average Cost Method, Specific Identification Method, FIFO Method

Starting in 2012, the fund will report the taxpayer's basis in the fund shares to the Internal Revenue Service (IRS) on Form 1099-B, Proceeds From Broker and Barter Exchange Transactions when the taxpayer redeems the shares. The reportable shares are called covered shares, whereas shares acquired before 2012 are noncovered shares. The fund will report to the IRS the average cost method for determining the basis for noncovered shares, even if the taxpayer uses a different method.

The basis of mutual fund shares = their cost + any load charges. However, if the taxpayer exchanges shares for similar shares in the same fund family and the load charge is waived, either wholly or partially, then the amount waived must be applied to the exchanged fund shares and not the original shares if the exchange took place within 90 days of the initial purchase. So if you invest $1000 in a mutual fund and paid $80 for the load charge, then your basis would be $1080. However, if you exchange the shares for other shares in the same fund family within 90 days, and the mutual fund waived $50 of the load charge for the exchange because of the recent purchase of the shares, then $30 of the initial load charge would be added to the original purchase, while the remaining $50 would be added to the basis of the exchanged shares. So the basis of the original shares would be $1030 and the cost basis for the exchanged shares would be $1050.

To calculate profit or loss, the taxpayer subtracts the basis in the shares from the redemption value. If the taxpayer purchased the shares all at one time, then there is generally no problem in calculating the basis. However, if the taxpayer acquired the shares at different times, and redeems some of the shares at different times, then a method must be selected that identifies which shares were sold so that profit or loss can be determined.

There are several common methods:

- average cost method

- specific identification method

- first-in, first-out (FIFO) method

You can choose which method to use or accept the fund's default method if no chose is made. However, if the average cost method is used, then it cannot be changed for the account. If any other method is selected, then the fund holder can usually choose another method later on. The average cost method is the most common method used:

Average Cost = Cost Basis of All Shares/Number of Shares

So if you bought 20 shares for $10 per share, then later bought 20 shares for $20 per share, then the average cost basis is calculated thus:

Average Cost = ($200 + $400)/(20 Shares +20 Shares) = $600/40= $15 per share

The average cost method is frequently used for bond funds, where price differences are minimal.

The 2nd method is the specific identification method, where the taxpayer specifically identifies which shares were sold. The specific identification method gives the taxpayer the greatest flexibility in regards to how much tax liability will be incurred and when, but the broker must be informed as to which shares were being sold and the taxpayer needs to receive written confirmation of those selling instructions.

The last method is the FIFO method, which simply identifies the redeemed shares as the 1st ones bought. Some funds may also use additional related methods, such as the last-in, first-out (LIFO) method, where the redeemed shares are considered the last ones purchased. Another method is the highest-in, first-out (HIFO) method, which identifies the redeemed shares as those with the highest basis, thus minimizing the tax on earlier sales.

Other less common methods may also be available. The low-cost method (LOCO method) selects the shares with lower costs, yielding the maximum gain or minimum loss. A taxpayer may want to maximum capital gain if the shares are donated to charity or if the taxpayer is in the 15% bracket or less. A polar opposite of the LOCO method is the high-cost method (HICO method), where the shares with the highest cost basis are selected for sale. There is also another method, the loss-gain utilization method, sometimes called the tax-sensitive method on some mutual fund forms, where higher-priced shares are sold that would create losses, then any remaining shares would be selected that would yield the best tax results.

If the taxpayer wishes to use a method other than the average cost method, then the broker must be informed of the method chosen, either in writing or online.

If the shares were received as a gift, then the donee should know the date of the gift, its fair market value on the gift date, the donor's adjusted basis, and in rare cases, if gift tax was paid on the shares.