Money

Money is something that is accepted as a form of payment for products or services, or for the payment of obligations. It is a medium of exchange with a specific value by which the value of all other things can be measured, which greatly facilitates trade and allows any economy to enjoy the benefits of the division of labor. Money made specialization practical; otherwise, it was more efficient for people to perform all the activities that they needed to survive. Money also serves as a store of value, so that money can be saved and invested for later use.

Barter

Without money, trade must be conducted through barter, where traders would exchange the things that they want less for things that they want more. The problem with barter is that it is difficult and time-consuming to determine the value of specific items. Additionally, most forms of barter cannot be broken down to buy things of lesser value, nor is it easily transportable. Barter also suffers from the requirement that the traders must have a coincidence of wants — that each trader happens to have what the other wants. Money solves these problems of barter. However, networks, including electronic networks, have made barter much more convenient, as evinced by modern-day Greece, which has been ravaged by an economic crisis for several years, depleting the country of euros for the everyday economy. So, many of its people have turned to barter because they do not have the euros to buy what they want: Why Greeks are ditching the euro for digital barter systems. Nonetheless, money is still more convenient than barter, as evidenced by the fact that it is only used when money does not hold its value (i.e., hyperinflation), or the supply is insufficient for the demand, as in Greece.

Money as a Medium of Exchange

Money is simply a common medium of exchange that everyone agrees upon, and, thus, they accept it as a form of payment for their goods and services. Money has 3 properties that make it desirable to use it as a medium of exchange. Money provides:

- a means of payment,

- a unit of account,

- a store of value.

However, these properties are desirable and effective only if the value of the currency is stable. While all currencies experience some inflation, most of this inflation is low and predictable. But if the value of currency fluctuates widely, then its utility as money declines dramatically. This is why Bitcoin will never serve as a currency for major economies and why virtually every country in the world has moved away from the gold standard and why they will never return.

Means of Payment

Money is an accepted unit of exchange for goods and services or for the satisfaction of obligations, such as debt, because it is standardized into specific units with specific values; hence, it is much easier to assess its value and can be readily exchanged. It is divisible into smaller units to make smaller payments, or large amounts of money can be carried with much less burden than carrying the equivalent value of barter. For instance, a $100 bill in American currency weighs no more than a $1 bill. Portability makes money convenient to use.

Unit of Account

Because money is standardized into specific values, it can be used to price goods and services, allowing the easy comparison of prices. Because the value of money is determined by general agreement, the condition of the money is irrelevant to its value. For instance, if a farmer wanted to buy a cow and offered a horse in exchange, then obviously, the seller of the cow would want to examine the condition and age of the horse since that would determine the value of the horse; likewise for the seller of the horse. When money is offered, only the amount matters, not its condition. Money must be fungible.

Prices provide information for consumers and producers who allocate economic resources to their most desirable uses. Items in demand command a higher price relative to the costs of the resources to produce them, which induces sellers to provide more of those items. Conversely, items with less demand have lower prices relative to their cost of production, and, thus, sellers allocate fewer economic resources to provide those items.

Store of Value

The value of money must be stable, keeping most of its value in time; otherwise, people would not accept it for payment. Money must be relatively scarce, so the supply of new money must either be difficult to counterfeit, or tightly controlled. Increases in the money supply must be gradual and expand with the economy. Otherwise, the increase of the total quantity of money will reduce the value of money, which is a direct cause of inflation.

The currency itself must also be durable; otherwise it would eventually lose its value as money as it decays or disintegrates, and, thus, people would not keep it.

Gold

The best example of money that illustrates its properties is gold. Gold is universally accepted by most cultures as a means of payment because it is relatively scarce, and new supplies are difficult to find and mine. As the most malleable and ductile of metals, it can also be easily cut into different sizes to correspond to specific values. It can be subdivided even more and still retain its value. It is also durable — it does not tarnish, corrode, or decay. Hence, it can be kept for a long time and still retain its value.

Commodity, Representative, Fiat, and Electronic Money

Money can be broadly classified as commodity money, representative money, fiat money, or electronic money.

Commodity Money

Commodity money has intrinsic value, such as salt in the Mediterranean region, silk in China, or gold and silver throughout the world, because these commodities have a value that is independent of its value as money. Gold, for instance, is extensively used in jewelry, and silver has many industrial uses.

Though commodity money is usable in some form other than as money, it also must satisfy the other characteristics of money. The commodity must be dividable into standardized quantities, so that different units of value can be created. It must be durable, so that it lasts; otherwise, it wouldn't function well as a store of value, and it must be continually replaced. Small size and light weight are desirable for easy transport.

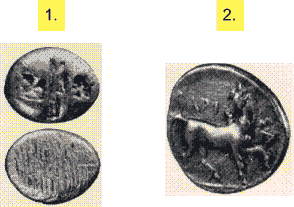

- Front and back of a Lydian Coin (Western Turkey), 700-637 B.C., which was the first known coin. Lydia was the first culture to issue coins for use as money.

- Coin used in Drachma, Thessaly (Eastern Greece), 400-344 BC.

Representative Money

Representative money is paper currency that can be exchanged for a fixed amount of a valuable commodity, usually gold or silver. Paper currency is convenient because it weighs little and much larger denominations can be printed that weigh no more than single units of currency. For instance, in 1715, Maryland, North Carolina and Virginia issued tobacco notes which could be converted to a specified amount of tobacco on demand, but were much easier to carry and to make large payments.

However, the acceptance of representative money depended on the reputation of the issuer. This is why the people in early America accepted banknotes, because the bank stood ready to redeem their notes in specie, which were gold or silver coins. However, some banks issued more notes than they had specie; when the public found out, they would run to the bank with their banknotes to redeem them before the bank ran out. Such runs on the bank, as they were called, occurred frequently in 18th and 19th century America, when many states poorly monitored the banks they chartered. Eventually, starting in 1861, the federal government started issuing its own notes, backed by government bonds held at the United States Treasury.

Fiat Money

Fiat money has no intrinsic value nor can it be redeemed for specie. Its value originates from government decree, or fiat. The best example of fiat money is paper currency. The paper itself has little intrinsic value, so fiat money can only serve as money if its production is tightly controlled. The production of fiat money is mostly controlled by governments. Governments maintain this control by using printing methods and materials that are difficult to reproduce, and by punishing counterfeiters with harsh penalties. For instance, in 12th century China, where the 1st paper currency circulated, the penalty for counterfeiting was beheading, and this was printed on the currency!

People use fiat money only if they believe that others will accept it as payment, and that it will not lose value. The government will also encourage using its money through the force of law, primarily by declaring it as legal tender. Legal tender is a form of money that must be accepted for the payment of debts and other liabilities. For instance since 1862, all United States dollars were printed with the phrase "This note is legal tender for all debts, public and private."

The issuance of paper money in the United States began in 1690, but the U.S. government did not issue paper currency with the intent that it circulate as money until 1861, when Congress approved the issuance of demand Treasury notes. All currency issued by the U.S. government since then remains legal tender, including silver certificates, which have a blue seal of the Department of the Treasury; United States notes have a red seal, and national bank notes have a brown seal. U.S. currency circulating today is as Federal Reserve notes with the green Treasury seal.

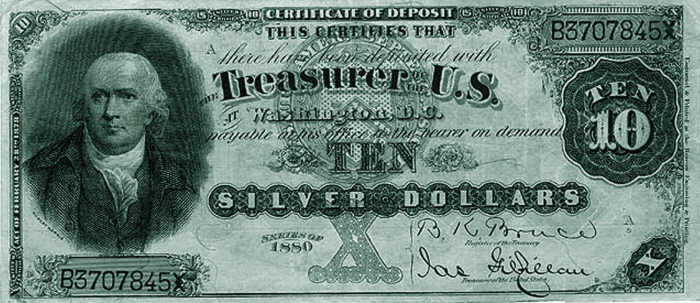

National bank note, Winters National Bank of Dayton, Ohio, printed in 1901. Note at the top middle of the currency's face the phrase "This note is secured by bonds of United States deposited with the U.S. Treasurer at Washington."

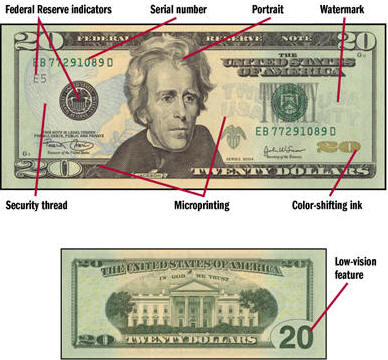

A modern 20-dollar Federal Reserve note illustrating the many details designed to thwart counterfeiting.

Electronic Money

Most money in most countries today exists only in electronic format, as records in the databases of financial institutions, so the United States Treasury no longer prints currency in denominations exceeding $100. Law-abiding citizens use checks or electronic transfers for large payments, while organized crime and terrorist networks use cash. Hence, the elimination of large denomination bills is considered a potent weapon against organized crime and terrorists by making it inconvenient and risky to transfer large amounts of cash. Some people have even suggested lowering the top denomination to $20 instead of $100; likewise, other countries, such as Europe, are also considering reducing their denominations since criminals often use currencies with the highest denominations. For instance, 1 million dollars in €500 bills weighs just 2.2 pounds, while the same amount in $20 bills weighs 50 pounds. Denominations exceeding $100 were last printed in 1945, but were issued until 1969 by the U.S. Treasury.

Eventually, when the technology costs less, all money will become electronic for its many advantages, both to governments and to the people. Coins have been around for thousands of years and paper money, for almost 300 years. However, these forms of cash are expensive to create, store, and transport, and they have security risks and costs. For instance, cash needs to be transported for businesses, people drive to and from ATMs to withdraw cash, and armored vehicles are frequently required to transport large amounts of cash from one location to another. Electronic money would obviate these and many other costs associated with physical money. Electronic money would also greatly reduce the tax gap, the tax revenue that the government could collect on income that is now either unreported or underreported.

Of course, a cashless society requires the technological infrastructure to support it, but with technological costs continually declining, and with the increasing ubiquity of smart phones, the necessary technology is either in place or available. The development of mobile payment platforms, such as Apple Pay and Google Wallet, and apps such as PayPal and Venmo are now paving the way for the cashless future.

However, electronic money can only exist with strong and stable financial institutions, because, like fiat money, its creation must be tightly controlled and people must be confident that it can work. A great impetus to make all money electronic is that it is the best way to stop organized crime and terrorism since electronic transactions are easily monitored and traceable, and tax authorities will certainly appreciate that tax evasion will be much more difficult. Of course, some people will be concerned about privacy, but most people are already giving up their privacy by using credit cards for purchases, by posting on social networks, and through other online transactions.

Money Creation in the United States

- Most money is created electronically and exists electronically, as records in electronic databases held by financial institutions, not as currency, but increasing the money supply is sometimes referred to as “printing money”, as this had been the primary way to create money before the electronics age and before the advent of checking.

- The Federal Reserve (the Fed) creates or regulates the creation of all electronic money.

- Currency and coins are minted by the Treasury Department's U.S. Bureau of Engraving and Printing, but the Fed determines the amount.

Cryptocurrencies

During the Internet age, privacy became important to many people, especially the privacy of their financial transactions. Furthermore, many people wanted to perform financial transactions without the mediation of a 3rd party, such as banks. Banks earned a bad reputation during the Great Recession of 2007 to 2009 since they were a major cause of the economic downturn.

In 2008, a white paper was published under the pseudonym Satoshi Nakamoto espousing a new type of currency using cryptographic techniques allowing financial transactions without a 3rd party, a peer-to-peer transaction where one party could send or receive money from another party directly, securely, and anonymously. This new currency was called Bitcoin, the 1st of the cryptocurrencies of which there are now thousands. Because Bitcoin was the 1st cryptocurrency and continues to be the most popular, the rest of this discussion will focus on Bitcoin, but most of what is said about it also applies to most other cryptocurrencies, especially regarding using cryptocurrency as money.

A cryptocurrency must solve several problems. The creation of cryptocurrency must be governed by strict rules to limit the supply, which is necessary for it to retain any value whatsoever. It must provide a way to transfer money from 1 party to another securely and keep a record of the transaction to prevent double spending, spending Bitcoins more than once by the same person. Transaction records must be secure from hacking so that they cannot be altered.

Bitcoins solve this problem by using a blockchain to create and store the Bitcoins and to record transactions. Blockchains are time-stamped, append-only logs that provide an auditable database, based on a consensus protocol. All Bitcoins and their transactions are stored in the blockchain, and nowhere else. People keep the cryptographic keys used to transact on the blockchain, but the Bitcoins and transactions exist only within the blockchain. Sets of transactions are stored in individual blocks that are encrypted, and some of the data encrypted in each block comes from the previous block, using hashing techniques that make it virtually impossible to alter any one transaction without altering the cryptographic integrity of later blocks. Furthermore, many copies of the blockchain are stored online in various places. New blocks are created and blockchains are maintained by people called miners, who must solve a cryptographic puzzle that will be used to encrypt the next block. The 1st miner to solve the puzzle earns some Bitcoin for their effort. The solution is used to encrypt the next block, then the other miners use the same key to encrypt the new block and add it to their blockchain. Minors also receive a fee for adding transactions to a block. The blockchain records transactions so that the same Bitcoin or other cryptographic tokens cannot be spent more than once by the same individual. A disadvantage of using a distributed ledger is that it takes longer to update transactions than updating a centralized database. Bitcoin transactions can take up to 10 minutes to verify, for instance, making it nearly impossible to process thousands of transactions per second if Bitcoin were used as a major currency. Financial networks in the United States, for instance, must handle up to 100,000 transactions per second. The Bitcoin blockchain can only handle 7 transactions per second, at best.

Money requires a stable value to be used efficiently. To maintain value, the supply of Bitcoins is limited to 21 million. Because economies have widely varying demands for money that changes over time, money that is strictly limited without regard to the needs of the economy will fluctuate widely in value, which greatly diminishes its usefulness as money. This is why Bitcoin continuously varies widely against government-issued currencies, such as the United States dollar. Thus, Bitcoin, or any other type of money with a limit on supply, will not be useful as money.

Without stability of value, a modern economy cannot operate. People cannot use it with confidence, without knowing what its value will be one year from now, one month from now, one week from now, or even tomorrow. Businesses need to calculate the present and future value of money to plan projects, yet without a stable value, present value and future value can never be calculated. 100 Bitcoins could be deposited in a savings account earning 5% interest to yield 105 Bitcoins at year-end, but those 105 Bitcoins will differ in value than 105 Bitcoins had at the beginning of the year; it could be less than 1/2 despite earning interest. There is simply no way to predict the future value. Some businesses may accept cryptocurrency to gain publicity, but no business can survive using Bitcoins or any other cryptocurrency as its sole type of money since it is impossible to run a business while its money fluctuates widely in value. This is why Bitcoin will never be used as money. It’s intrinsic value will always be 0; cryptocurrencies do not even have fiat value, so they cannot be used to pay for government liabilities, like taxes.

Money is stabilized by regulating supply. Most major economies have central banks that regulate the money supply. A central bank can increase or decrease the money supply for the needs of the economy. If there is too little money for the economy, then the money becomes more valuable, so people hoard it, thereby contracting the economy. This is the primary disadvantage with any type of currency in limited supply, be it gold or cryptocurrency.

While it is true that the supply of fiat money can be abused, most modern economies have solved this problem by making the central monetary authority, usually central banks, relatively independent of politicians. So that people maintain confidence in the government-issued currency, central banks usually state what their goals are regarding the money supply, which typically includes low-inflation and high employment.

When the economy contracts, the central bank can lower interest rates and increase the money supply simply by creating more money, then using that money to buy government debt securities, such as US Treasuries in the United States. When the economy is overheating, then the central bank can contract the money supply, which throttles the economy to a safer pace.

Such regulation of the economy is impossible if the money supply cannot be regulated. This is why the United States and every other country of the world has left the gold standard and why cryptocurrencies will never be a major currency for any major economy.

Another disadvantage of cryptocurrencies is that the government does not benefit from seigniorage, the profit from the creation of money, which can be substantial. For instance, in 2021, the United States supply of M2 money was about $20 trillion. If the US increases its money supply by 3% annually, that is an extra $600 billion annually that would otherwise have to be collected from taxes.

Cryptocurrency enthusiasts often argue that the main benefit of cryptocurrency is that it is independent of any government. However, governments can control cryptocurrencies. For instance, China prohibits cryptocurrencies entirely. And while blockchains may be secure against undetectable alterations, governments can easily cut off access to blockchains. Governments can also pass laws requiring the organizations or people supporting the cryptocurrency infrastructure to require identification of all users of the cryptocurrency. Blockchains located outside of the country can be blocked within the country. The need to collect taxes requires that the government know people’s income and spending; otherwise, governments cannot survive. While anarchists may laud that, modern civilization cannot exist without government.

If not useful as money, what causes demand for Bitcoins or for other cryptocurrencies? Much demand comes from criminal enterprises who are willing to accept the volatility of Bitcoin because financial transactions and money laundering can be done more covertly, making it easier to evade the authorities. People in countries with unstable governments or distrusted governments may also turn to cryptocurrency since it is better than using a hyperinflated currency issued by a corrupt government. Another source of demand comes from people hearing about the cryptocurrency and who want to try it. Most of these people purchase only a small fraction of a Bitcoin, but the demand created by many people around the world trying out Bitcoin may lead to a big demand overall, causing its price to increase.

Bitcoin and other cryptocurrencies even rise when they are mentioned in the news or when they are mentioned by a celebrity. On January 29, 2021, when Elon Musk added #Bitcoin to his twitter profile, Bitcoin surged 15% within minutes. Of course, this does not prove a cause-and-effect relationship, but it would not be unreasonable to suspect such a relationship.

The most prominent factor increasing demand is hype. Celebrities and other influential people may buy some cryptocurrency, then promote it among their followers on twitter or through other social media to increase its price, allowing them to sell for a substantial, easy profit. Needless to say, many people will be big losers since it is a zero-sum game.

Indeed, Bitcoin is the perfect scam, the perfect penny stock, the perfect pump-and-dump scheme. Bitcoin was not created as a scam, but the fact that its price depends on demand for Bitcoin and only on that demand, means that the price will only rise if people invested in Bitcoin can convince others that it has value. No regulatory authorities are currently restricting this type of activity, and indeed, it would be difficult to prevent. People can buy Bitcoin anonymously and sell anonymously, unlike with penny stocks where trading networks are legally required to store records of all transactions, which can be examined by the legal authorities, such as the Securities and Exchange Commission in the United States. The only purpose for buying Bitcoin or any other cryptocurrency is simply to sell it later, hopefully for a higher price.

Inflation

Inflation results when the money supply increases faster than the economy expands, resulting in higher prices. Sometimes, governments increase the money supply as an easy way to solve fiscal problems, but too much inflation can destroy the value of money. Inflation does the most damage to money as a store of value since its value continually declines as more money is created. Rather than keeping an inflating currency, people spend it quickly before it loses value, which, in turn, causes prices to rise even more.

Inflation also limits money as a unit of account because continually increasing prices makes it more difficult to compare the true value of goods and services.

Bitcoin Does Not Hedge Inflation

As you can see in this graph, Bitcoin does not hedge inflation. Since 2012, Bitcoin has dropped in price, sometimes substantially, even as the consumer price index continually increased. Of course, after the start of the Covid-19 pandemic, the price of Bitcoin increased rapidly, but it may not continue. Since Bitcoin cannot be spent, it must be sold to convert it into fiat currency. Few businesses accept Bitcoin for payment and few people use Bitcoin for payment because it is too volatile. Volatility complicates accounting, so most businesses would not want to transact in Bitcoin. A good hedge against inflation rises with inflation, such as real estate. Because the price of Bitcoin depends on hype and how much cash people will need, it will not serve as a good hedge against inflation. In fact, when inflation is spiking, people are more likely to sell Bitcoin to convert to cash to pay the higher prices, causing the price of Bitcoin to decline as inflation increases, the exact opposite of expectations.

However, Bitcoin can hedge against the inflation of a currency issued by a corrupt government, such as Russia. Indeed, both Russians and Ukrainians have been buying more Bitcoin and stablecoins, especially Tether, because the value of the ruble has plummeted, decreasing even more since the start of the Russian-Ukrainian war and the imposition of the many sanctions being imposed by the rest the world on Russia.

Finally, if inflation is too high, then people stop using it as a medium of exchange, and start using barter or the currency of another country or maybe even a cryptocurrency, such as Bitcoin.

One reason why there is more United States currency outside of the United States than within is because many people in certain countries do not trust their governments. They are afraid that their government will print too much money as an easy way to solve fiscal problems, which would reduce the value of the native currency held by the people. This happened in Argentina in the 1980's and in Russia in the 1990's. Hence, many of these people hold their store of value as United States dollars, mostly as 100-dollar bills.

Dollarization is the most extreme form of currency failure, when people lose all faith in their currency and adopt the currency of another country. Usually, United States currency is adopted because it is considered 1 of the safest currencies in the world, and because many United States immigrants send U.S. currency to their relatives abroad. Most recently, in 2000, Ecuador and El Salvador adopted dollarization as a policy.

The Value of Money Must Be Stable: The Problem with Using Bitcoin and Gold as Money

Inflation can be problematic, but it is usually predictable. What is worse is a currency that can fluctuate up and down unpredictably. Ron Paul, a US Congressman, wants to go on the gold standard because its supply cannot be abused by the government. Gold has been, and still is sometimes used as money. Bitcoin is a new type of money based on cryptography, where supply is limited by its own rules. Though gold and Bitcoins are sometimes used to pay for goods and services, they are most often held as speculative investments and as a hedge against inflation.

The supply of gold and Bitcoins is limited, so they cannot serve as money in most modern economies, because their value fluctuates considerably. Over the span of 1 year, the US dollar value of Bitcoin has varied from $5,000 to over $48,000. Likewise, gold has reached almost $2000 an ounce, only to drop back to around $1200 an ounce. In 2026, the price of gold has exceeded $5,300!

People will only use money if they have confidence in it. When a medium of exchange fluctuates wildly in what it can be exchanged for, it cannot serve as a unit of value or as a store of value. For instance, if you earned your money in Bitcoins and you wanted to save for a car over a 2-year period, then at the end of that period, you would not know if you had enough money to buy a Rolls-Royce or a scooter. Bitcoins, like gold, cannot serve as a unit of account, because it would be like trying to measure the length of objects using a tape measure where the length of its units continually changed. Imagine trying to conduct a business, for instance, without knowing what the value of your financial assets or your accounts receivable will be in the next month, let alone the next year.

Supply is unpredictable and will diminish over time. All Bitcoins are stored in the blockchain, the distributed ledger that records all Bitcoin transactions. Users of Bitcoins have private and public cryptographic keys that allow them to transfer their Bitcoins to others. Passwords are used to store the keys securely on various devices. If they lose those keys or passwords, then the Bitcoins associated with those accounts will be lost forever, without any way to ever recover them, thus contracting the money supply. Because the number of Bitcoins is limited to 21 million, the total number of Bitcoins will diminish over time, because it will be inevitable that people will lose their keys or passwords. Even if most of these keys are associated with a small fraction of a single Bitcoin, many people will lose their keys over time, and this process will continually contract the money supply, which can wreak havoc on any economy using Bitcoin as a currency.

Even using Bitcoins as a means of payment can be problematic since most people would want to look up the current exchange value before engaging in a transaction, thus complicating even simple transactions. Moreover, the value of Bitcoin could change significantly between the time that someone receives it as income and the time that it is spent, making financial planning impossible.

Being able to manipulate the money supply is hugely beneficial, so the gold standard was abandoned by every country years ago. An economy needs a certain amount of money to function properly, to keep values steady. Though inflation decreases the value of money, inflation is kept steady by the central banks, so it is largely predictable. If the central banks could not create or destroy money as needed, the value of currency would fluctuate with economic conditions. Indeed, because gold and Bitcoins can sometimes increase in value, people will often hold onto their money, hoping that its value will increase even more, just as the Japanese people have held on to their money in their deflationary environment, a major cause of their "lost decade".

To serve as a convenient means of payment, as an unit of account and as a store of value, the creation and destruction of money must be carefully controlled for the needs of the economy. If both the creation and destruction of money cannot be regulated, then the money itself will fluctuate in value, reducing its value as money and reducing the efficiency of the economy because the exchange rate of the present value of costs and revenue with their future value will be unpredictable. Present value and future value of investments is used extensively by investors to decide which investments are best and by businesses to decide which capital investments would yield the best returns. The calculation of the present value and future value of anything requires not only an interest rate but also a stable unit of money that will not vary unpredictably in value; otherwise, any calculated present value or future value will be meaningless. If I have 100 Bitcoins earning 5% annually, then, at the end of 1 year, I will have 105 Bitcoins. But how much those 105 Bitcoins will be worth 1 year from now is anybody's guess.

Certainly, the government can abuse the printing of money, but the government can abuse many things, such as can be seen perpetually in Russia. Only the people can ensure that the government works for their best interest. But an efficient economy requires money that not only serves as a convenient unit of exchange, but also as an accurate unit of account and as a predictable store of value. So, Ron Paul's desire to end the Fed and go back to the gold standard will never happen. Likewise, Bitcoins will remain a speculative investment.

Will Bitcoin Keep Rising in Price?

Cryptocurrency enthusiasts are continually striving to solve the problems with cryptocurrency. A major problem with Bitcoin and other cryptocurrencies is that it takes considerable time to process transactions. One solution was to increase the block size of the individual blocks in the blockchain, so that more transactions can be processed in a batch. However, this can also slow the network and require more time to accumulate enough transactions to fill the block. Another potential solution being proposed is the Lightning Network, where people who frequently transact with each other can establish a tab of a certain amount recorded in the blockchain, but then use that tab to transfer money using a localized process that does not depend on updating the blockchain. Only when 1 of the users terminates the relationship will the blockchain be updated and any remaining funds released to the appropriate parties.

The problem with these solutions is that they are placing the cart before the horse. The fundamental problem with cryptocurrencies is the supply problem, which causes wild fluctuations in price. To be practical as money, any practical currency would need a stable value; without that, any form of money would not be practical as a means of payment, as an account value, or as a store of value for a major economy, or even for a major organization. Though Bitcoin seems to be attracting more and more followers — even businesses are starting to dip their toes in the Bitcoin universe — it still cannot become a major currency without a stable value.

Some people have tried to address this issue by creating what are called stablecoins, but this solution also has its problems. One solution to stabilize stablecoins is to establish a 1-to-1 correspondence with a fiat currency, such as the US dollar. However, that would require a central authority who can control the supply of stablecoins while standing ready to exchange the stablecoins for a fiat currency. But stablecoins have no fiat value, so few people accept it as a means of payment.

So, for instance, if someone stood ready to exchange a stablecoin for a US dollar, then anybody who had stablecoins would quickly exchange them for the US dollar since the US dollar has fiat value but the stablecoin does not. Furthermore, why would anyone even want stablecoins? The main reason why Bitcoin is so popular today is because people are buying it hoping to sell it for a higher price later. Without that profit incentive, there is no apparent reason to even buy stablecoins.

To summarize, no cryptocurrency could ever be practical as money if it does not have a stable value, but if its value is stable, then no one would buy it because there would be no reason to get a cryptocurrency with no fiat value. Furthermore, using cryptocurrencies extensively in any major economy would eliminate some of the monetary policy tools that central banks use to regulate the economy. For instance, the Covid-19 pandemic would have damaged the economy to a much greater extent, if central banks could not increase the money supply. For the same reason, it would’ve taken the world much longer to recover from the Great Recession of 2008.

Creating and destroying money is required to stabilize the value of that money, because supply and demand for money continually fluctuates. But the creation and destruction must be done by a central authority that is not exposed to the whims of politicians or where such influence is limited. Moreover, if money cannot be created, a deflationary spiral will occur as the economy grows and requires more money to operate, causing people to hoard the money as it increases in value, which will severely damage the economy.

The biggest problem with cryptocurrencies is that they do not solve an exigent problem. Most people are satisfied with fiat currencies and while financial transactions can be tracked, most people who are not criminals don't worry about that. The other problem that will occur if cryptocurrencies gain currency, so to speak, is that governments will require information about financial transactions to ensure the collection of their taxes, for instance. This is one reason why organizations must report cash transactions exceeding $10,000 in the United States to the IRS. Cash already has an anonymous feature, but few people use it. Even though most people could use cash, most people choose to use credit cards and bank transfers for their convenience.

Most of the supposed benefits of cryptocurrencies spring from being simply an electronic means of payment, but most fiat currencies are also electronic money: most transactions in modern economies are entirely electronic. Limits on fiat currencies are imposed by law or by businesses, which can easily be changed. For instance, a US dollar or a euro can easily be subdivided into any number of smaller units if the government allowed it, and it is my prediction, that they will soon allow it. Some cryptocurrency enthusiasts argue that crypto-transactions will be cheaper. They say, look at credit card transaction fees. The problem here concerns the establishment of businesses and oligopolies that process fiat currencies. For instance, 1 of the reasons why credit card transaction fees are so high is because an oligopoly controls that, but the government can take steps to increase competition, and in many places, that is happening. Furthermore, most cryptocurrency transactions also have significant fees. So, in my opinion, fiat currencies will continue to reign supreme because they work, and they are convenient.

Volatility will increase not only for its limited supply, but because cryptocurrencies do not have fiat value, so they must be converted back to fiat currency to be spent, further increasing its volatility. Though some businesses advertise that they will accept Bitcoin as payment, few businesses could withstand the extreme risk of a sharp decline in prices, so paying in Bitcoin will always be extremely limited.

Another factor that may cause a sharp decline in prices is the proliferation of other cryptocurrencies. Many people will either buy the much cheaper cryptocurrencies or sell Bitcoin to buy those currencies, hoping that cheaper cryptocurrencies will increase in price faster than Bitcoin. However, virtually all cryptocurrencies use much of the same underlying foundation to operate as Bitcoin, and none of them really provide any significant advantage over fiat currencies, while still having significant disadvantages.

So will Bitcoin continue to trend upward? As of 2025, it has exceeded $111,000. It could even reach $1 million or more. I say this as a possibility, not as a prediction! This possibility is plausible because, just in the United States, the money supply exceeds $20 trillion, so, much more than that must exist in the rest of the world, and since the Bitcoin market is global, 21 million Bitcoins, the maximum possible per its rules, would yield a value of $21 trillion, which would still be a small percentage of the total global money supply.

Though it has no real value, many people continue to think that it will continue to rise. So long as enough people continue to think that it will rise ever higher, then it will keep rising. Of course, the higher it goes, the greater the risk of buying it. But because there will only be 21 million Bitcoins, many of them already lost through lost keys and passwords, there is still enough hype circulating online and in the news to keep it ascending sporadically, sharply rising up and down, but trending upward. As it ascends ever higher, more speculators will be drawn in. Even companies will get in on the act, at least for a while, because as the hype keeps increasing, Bitcoin will keep rising — until it doesn’t.

What is the top price? Nobody knows. If somebody says they know, just remember: they don’t. Even if that somebody is a major bank. Eventually it will crash. Anyone, who clearly understands the disadvantages of Bitcoin as a unit of money and that it would eliminate a powerful monetary tool for regulating the economy, will realize that, at some point, it will fade! Its volatility will be horrendous. Many may be borrowing money by mortgaging their homes or taking cash advances on their credit cards to bet on this speculative bubble. However, sharp price drops will force many people to exit at once, causing even greater price drops. Eventually, it will stabilize, then rise and decline again — who knows for how many cycles — maybe hurting the economy if too many people borrowed money to bet on Bitcoin. If economies are damaged too severely, then governments will step in to regulate the cryptocurrencies.