Primary Corporate Bond Market

There is a primary market for both government bonds and corporate bonds. The primary market for most government bonds is determined by the type of government bond. The largest bond market is for United States Treasuries, which is presented in Primary and Secondary Markets for United States Treasury Securities. This article presents the workings of the primary market for corporate bonds.

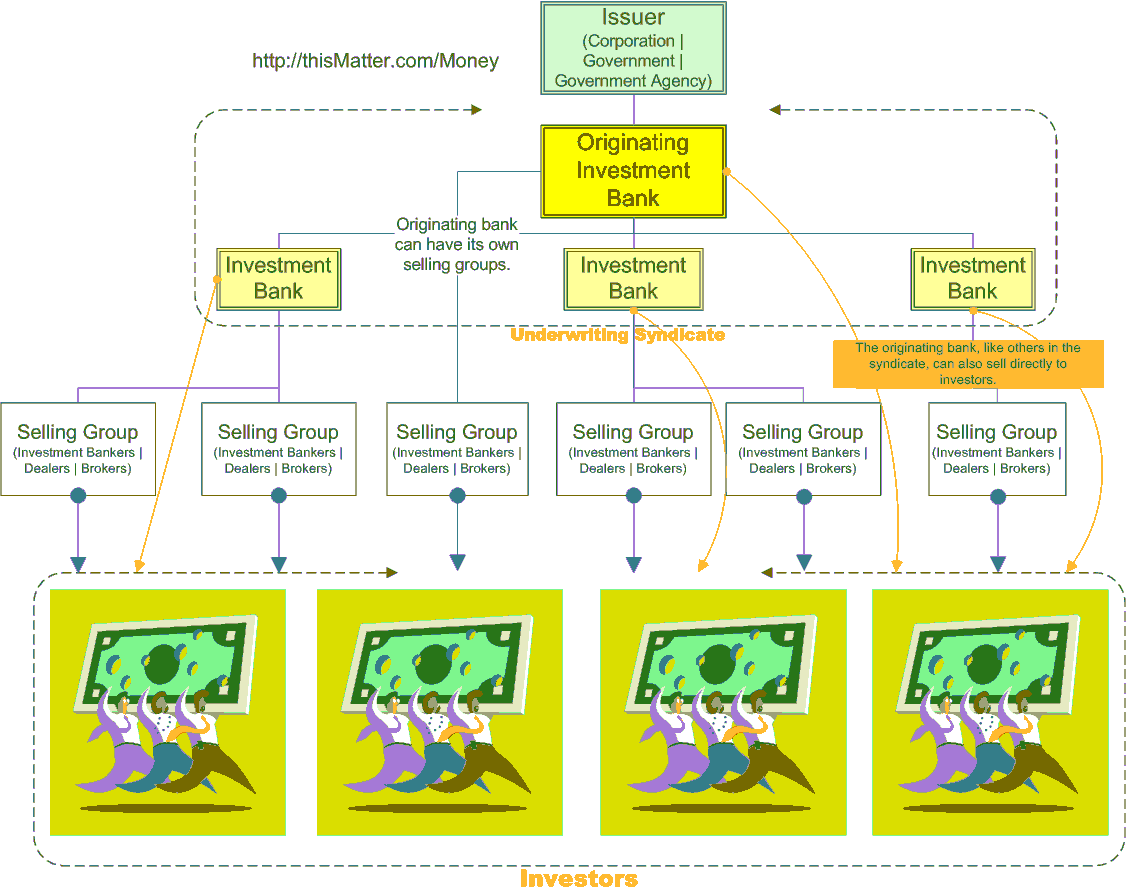

The creation of corporate bonds is like the creation of stocks. Generally, a firm that wants to issue bonds will go to an investment bank for one or more of these services:

- expertise and advise in creating the issue, including determining the yield and maturity;

- the investment bank may buy the whole issue as firm commitment underwriting, or may use a best efforts approach to sell the bonds;

- the investment bank may form a syndicate and/or a selling group to help sell the bonds to their institutional investors and to the public.

The sale of newly issued bonds to the public constitutes the primary bond market; most of the money received in the sale of the primary issue goes to the issuer. The reselling of bonds by investors constitutes the secondary bond market. The money paid for bonds in the secondary market goes to other investors, not to the issuer.

The investment banks profit by selling the bonds for more than what they paid for them, which is the underwriting discount or gross spread.

The Securities Act of 1933 requires that securities offered to the public must be registered with the Securities and Exchange Commission (SEC). Information that must be provided in the registration includes the nature of the business, features of the security being offered, potential investment risks, a profile of management, and a list of major investors. Financial statements, certified by a public accountant, must also be provided, and must comply with U.S. generally accepted accounting principles (GAAP).

The registration has 2 parts:

- the prospectus, which is publicly distributed, and

- supplemental information, which is available to the public upon request.

When the registration is approved by the SEC, the securities can be offered for sale to the public.

Bond Underwriting

As described, the underwriting of corporate bonds is like the underwriting of stocks (for more detailed information, see Investment Banking — Issuing New Securities), but sometimes bonds are brought to market by different methods.

Bought Deal

An investment bank offers a firm commitment to buy a specific number of bonds at a specific price for a specific yield and maturity from the issuer. If the issuer accepts, then the investment bank has a bought deal. A bought deal is good for the investment bank because it gives the bank time to form a selling syndicate or selling group to share the risk of the underwriting process. Often, the bank borrows money to finance the bought deal. Usually the investment bank will distribute the bonds to other investment banks in the syndicate or the selling group to sell to the public, and to institutional customers who have expressed or may have an interest in the bond issue.

Competitive Bidding Underwriting, or Auction Process

Often, auctions yield the most money for the issuer and also allow the issuer to sell directly to the public or institutional investors, eliminating the underwriting fee. Regulated public utilities and some municipalities must use this method. The U.S. government sells Treasuries using auctions.

How the bid is made depends on whether the issue is being sold at a discount to par value, or as a bond paying interest. If the bid is for a discount bond (also called a zero-coupon bond), like federal T-bills for instance, then bidders offer the price they are willing to pay, and the issue is sold to the highest bidders. If it is bonds paying interest, then bidders specify the yield that they are willing to accept. Winning bidders will be those willing to accept the lowest yields since this is the interest that the issuer must pay for the borrowed funds.

Depending on what type of auction it is, a bidder can bid for the entire issue or just part of an issue. In a bid for the entire issue, the issuer publishes the terms of the issue, then investment bankers bid for the entire issue, who then sell the bonds to their customers, making money from the underwriting spread — the difference in price that they paid for the issue and what they sell it for to investors.

In a competitive bidding for parts of an issue, bidders submit the yield that they are willing to accept, or the price that they are willing to pay, and the amount of the issue that they want. Example: Bidder A might offer to buy $100,000,000 worth of bonds that pays 5.1% interest. Bidder B might offer to buy $40,000,000 worth of bonds that pay 5.2% interest; Bidder C might want $10,000,000 for a 5.2% yield. How the bonds are then distributed depends on whether it is a multiple-price auction or a single-price, or Dutch, auction.

In a multiple-price auction, the winning bidders pay the price that they bid for the amount that they requested. If there is an equal bid among bidders, but not enough shares to sell, then each bidder will get a part of the remaining shares that is proportional to the amount that they requested.

In the above example, suppose the issue to be sold consisted of $110,000,000 worth of bonds. Bidder A would get all $100,000,000 worth because Bidder A was willing to accept the lowest yield. Now with only $10,000,000 worth of bonds left to sell; Bidder B wanted $40,000,000, Bidder C wanted $10,000,000. Bidder B would get $8,000,000, because 40/50 = 8/10, $50,000,000 being the sum of both bidders initial amount. Bidder C would get the remaining $2,000,000 worth of bonds.

In a single-price auction, or a Dutch auction, all winning bidders will receive the highest winning yield, or in the case of a discount bond, will pay the same price. Thus, in the above example, Bidder A, B, and C would get a 5.2% yield for their bonds, because 5.2% was the highest yield the issuer had to offer to sell all the bonds.

In 1997, issuers started using online auctions to sell directly to investors to save on investment banking fees. In fact, the U.S. government has a website at https://TreasuryDirect.gov allowing virtually anyone to buy Treasuries directly. Investment bankers argue that they can get the lowest price even after accounting for the underwriting fee because they know their customers, and they make secondary markets in the issue, improving liquidity. However, no studies confirm this.

Medium-Term Notes

Medium-term notes are corporate bonds registered with the SEC as a Rule 415 shelf registration, which allows the corporation to register up to $1 billion worth of bonds at one time, but which are then offered in relatively small amounts continually by agents of the issuer as the need for money arises over a 2 year period. The rates are chosen by the issuer with various maturities, and are usually expressed as a spread above U.S. Treasuries of comparable maturity. Terms for a given yield range from 9-12 months, 12-18 months, 18-24 months, up to 30 years, but could even be for 100 years. The issuer's agents, usually investment banks, publish an offering rate schedule for institutional investors using a best efforts sales approach. The institutional investor can choose, with the issuer's approval, a final maturity date for a given issue.

Reverse Inquiry: Customizing Tranches to the Needs of Specific Institutional Investors

A shelf registration also allows the issuer to issue bonds with different coupon rates and maturities as separate tranches. In a reverse inquiry, the investment banker, acting as an agent of the issuer, learns the needs of his institutional customer, and tailors a tranche to meet the needs of that customer.

SEC Rule 144: Private Placement Market

Companies too small or risky for an IPO can get financing through private placements, which is also cheaper and faster than a public offering. SEC Rule 144 governs private placement transactions.

A private placement is the selling of unregistered securities, either stocks or bonds, to qualified institutional investors — investment companies, pension funds, and insurance companies, especially life insurance companies. The cost of a private placement is much less than a public offering, because the securities do not require SEC registration, the issuer does not have to comply with U.S. GAAP, and with usually only a few institutional investors involved, marketing costs are much less.

The SEC enacted Regulation D in 1982 which defines a qualified institutional investor as one who can understand, or can employ those who understand, the return and the risk of securities, and can bear the risks.

However, the purchaser of a private placement must sign a letter of intent, called an investment letter, which states that the securities are being bought for investment and not for resale. Thus, these securities are often called letter securities, or in the case of bonds, letter bonds. If the letter securities are stocks, then they may be called letter stocks, or 144 stocks.

The issuer need not give a prospectus to buyers in a private placement, but it still must furnish information that the SEC deems material as a private placement memorandum to potential investors. Unlike a prospectus, though, the SEC does not review the memorandum. With fewer investors for private placements, the investors can usually negotiate the characteristics of the issue, giving them more flexibility than they would have in a public offering.

Letter securities cannot be resold for 2 years (1 year if more onerous conditions are met), and when they are, it must be a regular brokerage transaction.

Most private placement bonds are not investment grade, and because they were privately placed, they can't be resold to the public unless they are first registered with the SEC. Thus, they generally pay a higher interest rate compared to other securities of comparable terms.

An investment banker can tailor private placements for their institutional customers.

Rule 144A: Increasing Liquidity and Foreign Investment, and Domestic Issuance of Foreign Securities

Previously, investors who bought private-placement securities could not resell them for 2 years. This cost issuers more because they had to pay a higher yield to compensate investors for the illiquidity of their purchase. In April, 1990, the SEC enacted Rule 144A, which allowed institutional investors to trade the investments among themselves at any time, and without having to register the securities. This not only lowered the cost of raising funds by the issuer, but it also increased foreign investment, which increased the money supply, thereby reducing its cost even more. Rule 144A offerings are underwritten by investment bankers.

Rule 144A also enhanced the domestic issuance of securities for foreign issuers, primarily because it eliminated the need to register the securities, thereby saving time and expense.

Secondary Bond Market

With many more bonds than stocks — about 800,000 bond issues compared to about 8,000 stocks traded on the New York Stock Exchange and NASDAQ — most bonds are traded over the telephone rather than on an electronic exchange. The diversity of bonds results from both more issuers and more issues of bonds with different characteristics, maturities, and yields, from each issuer. The illiquidity of most bond issues also makes it difficult to list current prices since the last trade for a particular issue may have been weeks or months ago. Changing interest rates or credit ratings can impact prices since the last trade. A bond trader can give a more accurate quote from knowing recent prices of bond trades with similar characteristics, which would be difficult to do with an electronic exchange. Rather than providing a best bid/ask prices for particular bond issue, an electronic system can facilitate trading by making it easier to get multiple quotes from bond dealers for a particular bond.

MarketAxess and TradeWeb are 2 electronic systems that allow prospective buyers of bonds to do just that. Though many Treasuries are traded using the U.S. Treasury's website TreasuryDirect, only a small portion of corporate bonds are traded electronically, though this number is sure to increase, especially for investment-grade corporate bonds.

Bond Trading at the NYSE, NYSE Bonds

The New York Stock Exchange Group, Inc. lists bond issues of all NYSE-listed companies on NYSE Bonds. The SEC had granted the NYSE an exemption to the rule that required that each bond be registered before it could be listed on an exchange. Exchange-listed bonds would have the more competitive bid/ask pricing system over the usual best-efforts approach where a bond broker would call 3 dealers to get the best price among them, even when there could be thousands of other dealers in the bonds — at least a few of whom would almost certainly have better prices. An exchange-listed bond price would aggregate all prices available for the bond into the best bid/ask price, like stocks and options are listed.

Trade Reporting and Compliance Engine (TRACE)

TRACE is a FINRA approved trade reporting system for corporate bonds trading in the OTC market. TRACE only reports trades: it does not provide execution, settlement, or clearance services. Trades must be reported by both sides of the transaction within 15 minutes of execution, and the report must include execution date, time of trade, quantity, price, yield, and if the price reflects a commission. Most corporate debt securities are eligible for the system, but not:

- mortgage and asset-backed securities, including collateralized mortgage securities

- money market instruments

- municipal securities

- foreign country and foreign government-sponsored debt

- convertible corporate bonds