Payment Systems

A payment is the flow of funds from the payer to the payee, usually as compensation for a product or service or to pay off a liability. Most personal payments involve the exchange of cash. Though money, as coin and currency, has served as the medium of payment for millennia, and continues to serve that purpose in most personal transactions, it is severely limited:

- it is not easy to pay someone who is remote geographically;

- it is inconvenient and insecure to issue many payments, such as an employer paying its employees;

- it has no inherent record of the transaction.

A primary purpose of banks is to provide a payment system. Banks solve payment problems by providing checking services and electronic funds transfers (EFTs) using 2 fundamental processes for both:

- an instruction to transfer money from one account to another

- then the actual exchange of money, where the payer's account is debited and the payee's account is credited

Accounts are nothing more than electronic records. With paper checks, the accounts are updated by an operator working at a computer terminal or read by optical character recognition software. With electronic funds transfers, updating accounts is entirely electronic, nothing more than updating records in databases, so it is faster and cheaper.

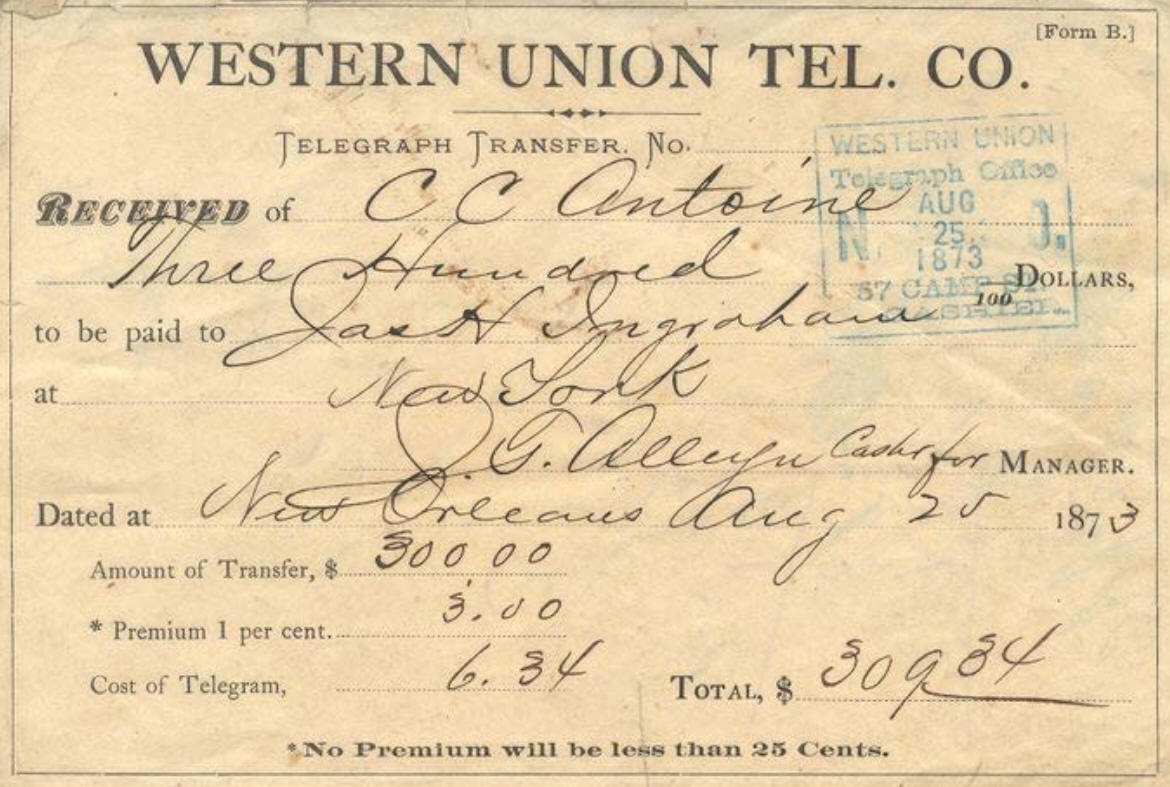

One step in most payment processes is the transfer of funds from the payer's bank to the payee's bank. To facilitate the transfer, each bank is assigned a unique routing number (aka routing transit number, ABA number), a number assigned by the American Bankers Association to a bank that uniquely identifies it like a social security number uniquely identifies an individual.

With paper checks, the payer's bank routing number and the payer's account number are listed at the bottom of the check in magnetic ink, which allows reliable optical character recognition of the numbers, expediting the delivery of the check from the payee's bank back to the payer's bank to account for payment. Before the payee's bank sends the check to the payer's bank, it stamps its routing number on the back of the check, so that the payer's bank knows where to send the funds.

With electronic funds transfers, all the required information — payer's bank routing number and account number, the payee's bank routing number and account number and the amount of the payment — are contained in the EFT message, so the payment can proceed without any human assistance, so EFT payments are much cheaper and faster than payments by paper check.

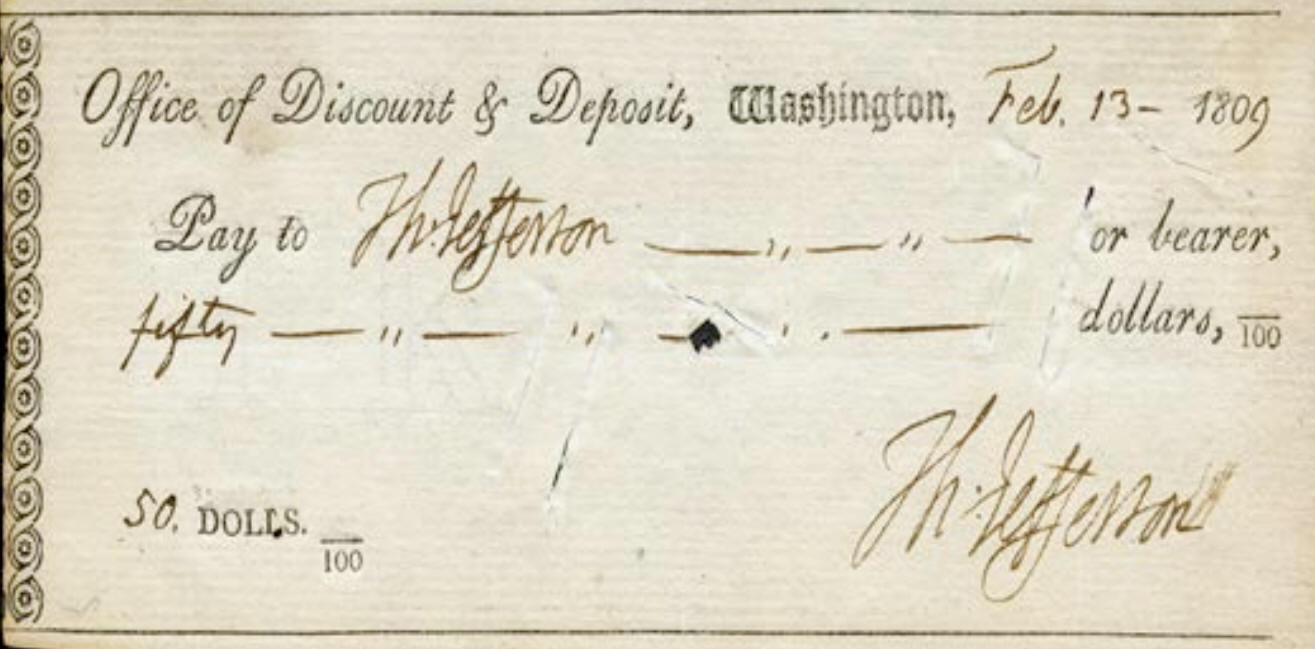

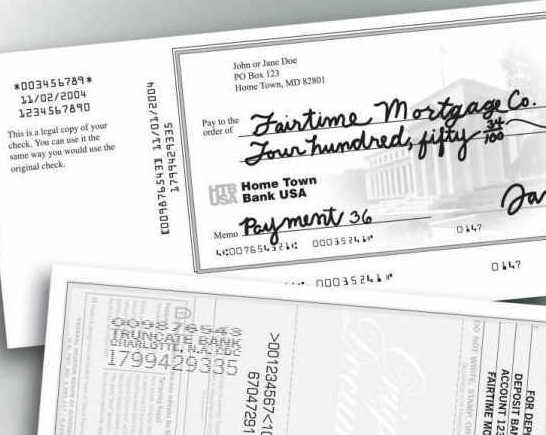

Checks

Because checks are paper documents, more steps are needed to complete a check-based transaction. Unlike currency, checks are not money but legal instruments instructing the bank to take money out of the check writer's, or the payer's, account and give it to the payee of the check. This involves debiting the payer's record at the payer's bank and crediting the payee's record at the payee's bank. Only then is the payment final.

Typically, the payee deposits or cashes the check at her bank. At the end of the day, the bank sends the check to a clearinghouse operated by the Federal Reserve or to a private clearinghouse, where both the payer's and payee's banks have accounts. The clearinghouse offers clearing and settlement services to its members, the participating banks. Clearing is the transfer of the check from the payee's bank to the payer's bank and the transfer of funds from the payer's account to the payee's account, and settlement is the actual adjustment of accounts that reflects the transaction, where the payer's account is debited and the payee's account is credited. The clearinghouse credits the account of the payee's bank and debits the account of the payer's bank. However, the transaction at this stage is only provisional since the payer may not have sufficient funds to cover the transaction. From there, the check is sent to the payer's bank, then the bank debits the payer's account. If the account has insufficient funds, the payer's bank returns the check, following the reverse order, through the clearinghouse, then back to the payee's bank. Historically, canceled checks were usually returned to the payer to give the payer a proof of payment. Nowadays, banks only provide electronic images of the checks, if the check writer requests it.

Not every transaction uses a clearinghouse. On-us payments are payments where the payer and the payee use the same bank, and also include ATM transactions by a customer using the bank's ATM.

In October 28, 2004, the Check Clearing for the 21st Century Act, aka Check 21, was enacted that gave banks the authority to save only the image of the front and back of the check and to transmit the image to clearinghouses and other banks instead of the paper check. Check 21 gives these substitute checks the same legal proof of payment as paper checks. Check 21 saves banks billions of dollars every year and reduces the time between when a check is deposited and when it is debited from the payer's account. (Source: https://federalreserve.gov/paymentsys.htm)

Electronic Funds Transfers (EFTs)

Electronic funds transfers (EFTs) are like electronic checks that automatically debit the payer's account and credit the payee's account. EFTs do not require clearinghouses because the routing information is in the electronic message.

EFTs require a secure network and operating standards. With various EFT networks, the most common type of EFT is the automated clearinghouse transaction (ACH), which many businesses and people use to pay recurring bills. The ACH Network is operated by the Federal Reserve and the Electronic Payments Networks, and most banks use this network like they used clearinghouses — to exchange payment information. An ACH transaction consists of the account numbers of the payer, the payer's bank, the payee's bank, the account number of the payee, and the amount of the payment. An ACH transaction has the same basic information on the payer as a paper check with its bank routing number and the payer's account number. It differs from the paper check in that it also has the payee's bank routing number and the payee's account number so it can be completed as a single transaction.

Some retailers, such as Walmart, can convert a paper check directly into an ACH transaction by scanning the check for the bank's routing number and customer's account number. The customer then signs and gets a receipt. This saves the retailer the cost and risk of transporting paper checks.

Another EFT network is Fedwire, which is operated by the Federal Reserve, and is used transfer large sums of money, mostly between banks and other large institutional customers. The Federal Reserve consists of 12 district banks in different areas of the country. Banks in the area have accounts at the local Federal Reserve. When they want to send money to another bank, they send payment information to their local Federal Reserve Bank, which then sends the payment information over the Fedwire to the Federal Reserve Bank in the payee's district, who then credits the payee's account for the amount of the payment.

The number of noncash payments — checks and electronic payments — has increased steadily throughout the world over the years. However, the proportion of payments as checks is continually decreasing, while electronic payments, as debit, credit, stored value cards, and ACH transactions, are continually increasing, both in absolute amounts and as a percentage of all payments, a trend that will continue.

Debit, Credit, and Stored-Value Cards

A common method to pay is by using debit and credit cards or stored-value cards (aka gift cards, prepaid cards, smart cards). All transactions involving cards require an electronic payment network. The cards have the payer's information and the payee's information is supplied at the time of payment. However, the payer's information may differ depending on the type of card used, because the payer is not necessarily the cardholder. A debit card works like a check, in that the cardholder's bank account is debited for the payment. However, the payer for a credit card is the issuing bank since the payment is a loan by the issuer to the credit card holder that is paid directly to the payee.

Another type of electronic payment is the stored-value card, where money, as account information, is stored on a card. Gift cards are the most common type of stored-value card. Prepaid cards, such as those issued by VISA, is also becoming more common. Stored-value cards allow customers with poor or no credit and no bank account to pay electronically.

However, the stored-value card still uses a bank account — that of the bank itself. When you pay to have money loaded onto a stored-value card, what is actually loaded is the account information that has been set up just for the card. When you purchase an item from a merchant with the card, the card is read by the merchant's card reader, which sends the account information over the network to deduct the payment from the account set up for the card and credits the merchant's account. So, a stored-value card can be canceled just like a debit or credit card if it is lost or stolen.

E-Money

An increasing amount of retail business is being conducted online, but the payment systems provided by banks have 2 deficiencies that reduce the value of their services to many online merchants.

- Current EFT systems do not provide a way for a person to send money to another person or to send it to a business lacking a merchant account that would allow it to accept credit and debit cards.

- Banks issuing the cards charge merchants a fee for each transaction, so cards are not a good way to sell items for a few cents, or even less than a penny — so-called micropayments.

With these deficiencies, many businesses have sprung up to provide payment services to satisfy these needs. Some have called these special services e-money, because purchases can be made online, but they differ from credit and debit cards, and other types of electronic payments provided by banks.

PayPal is a major business that allows people to send money to other people or to merchants without a merchant account with a bank. The way PayPal usually works requires that the payer and payee both have accounts at PayPal. The money is initially transferred to the PayPal account by debit or credit card or by an ACH debit from the account holder's bank account. Each account is designated with an email address. So if a person wanted to send money to another person, the payer only needs the email address of the payee, then the payer sends payment instructions to PayPal that includes the amount of the payment and the email address of the payee: no fee to make payments but fees are charged for receiving payments, which makes PayPal unsuitable for micropayments.

Currently, no prominent companies offer micropayments that are widely accepted, although cryptocurrencies, such as Bitcoin, are starting to be used as such. However, advancing technology should decrease the cost of using the traditional payment networks, including debit and credit cards, which would obviate the need for a special micropayment network or for cryptocurrencies.

Bitcoins and Cryptocurrencies Will Never Be Major Currencies

Another form of payment receiving media attention recently is Bitcoins or other cryptocurrencies. Some of the main advantages advanced for Bitcoin are that:

- the supply is strictly limited and not controlled by the government

- Bitcoins can be subdivided indefinitely into smaller payments, allowing for micro-payments, and

However, some of these advantages touted for Bitcoin result because it is an entirely electronic form of money. If the United States dollar or the euro was made entirely electronic, then those currencies could be subdivided indefinitely to allow for micro-payments. Most fiat currencies have a lower limit for value because they are represented by coins and paper currency, which cost money to produce. Indeed, the US penny and nickel cost more to produce than their fiat value. On the other hand, the value of electronic money can be reduced, virtually without limit, to form smaller payments.

When money becomes entirely electronic and the government institutes reforms to exploit electronic payments — which I believe is inevitable — then all the advantages of electronic payment, such as enabling micro-payments and lowering transaction costs, will be realized for that currency.

That the supply of Bitcoin is limited is actually a major disadvantage since the value of Bitcoin varies widely over short periods because supply cannot be increased or decreased to meet changing demand. So, Bitcoin and other cryptocurrencies, or for that matter, any other means of payment, such as gold, where the supply cannot be controlled, cannot satisfy the primary functions of money as a unit of exchange, unit of account, and store of value.

Using cryptocurrencies as a unit of exchange is very risky. Imagine if Walmart or Amazon accepted Bitcoin for payment. What would happen to these companies — or any other company — if the value of Bitcoin suddenly dropped to half its value or more, as it has already done? In December 2017, the price of 1 Bitcoin reached almost $20,000. Shortly afterward, near the start of 2018, the price of Bitcoin was less than $9,000 (USD)! The pay rate for employees would have to change every week and prices paid to suppliers would have to change with every payment. This would be a managerial nightmare!

It cannot serve as a unit of account because its varying value, even within a short time, makes its exchange value for goods and services unpredictable; price comparisons would be impossible because these cryptocurrencies vary in value by the minute, so any prices you would see may be stale, reflecting the value that Bitcoin had at an earlier time. Likewise, it cannot serve as a store of value since it can lose value very quickly, as has already occurred several times with Bitcoin and many times with gold. Additionally, using methods common in business and investments, such as calculating the present value or future value of projects or investments or even calculating financial risk, becomes impossible. Calculating present or future value is only meaningful if the currency's value is stable. Even though most currencies decrease in value from inflation, inflation is usually low and predictable, so it is easier to adjust.

Hence, Bitcoin or any other type of money where the supply cannot be controlled will never serve as a major currency or co-currency. Instead, Bitcoin will remain as it is, a novelty currency that can be used either as a medium of exchange for those businesses or individuals willing to assume the risk of a widely fluctuating currency or to profit from speculation, where profits are contingent on the greater fool theory. Because the intrinsic value of Bitcoin and other cryptocurrencies is 0, that is the price that I believe it will eventually fall to, though it may take many years.

(Another factor propping up the prices of cryptocurrencies far beyond their intrinsic value is micro-demand. Because cryptocurrencies can be subdivided into ever smaller amounts, I believe many people are getting these small amounts to experiment with these novel currencies. When the demand for these micro-amounts is totaled over the entire global population, the result is significant demand. Eventually, people will realize that cryptocurrencies offer no added value over traditional forms of electronic payments, nor are they spendable at most places, so, it is still my prediction that all cryptocurrencies will drop to their intrinsic value of 0, though it may take years. Blockchain, of course, has great promise, but this is used only to record transactions. Though Bitcoin and other cryptocurrencies depend on blockchain, blockchain does not depend on the cryptocurrencies.)

Future of Money

Soon there will be many more ways of payment. For instance, in Asia and Europe, people can pay using their cell phones by waving the phones in front of special electronic readers, which transfers banking account information. However, these forms of payment are just special forms of the EFT payment system described above.

Financial transactions are increasingly becoming electronic since settling transactions electronically saves both time and money. The advantages of electronic money are that it is much less apt to be lost or stolen and it will become more convenient as the technology improves. The big disadvantage is that there is no privacy. Where you go and what you spend money on will be listed in databases on some network. Governments can construct a profile of you simply by aggregating this information, which is trivial with today's technology.

Money as coin and currency may disappear entirely when payments become totally electronic. However, the units of money will still be needed as a unit of account so that the prices of goods and services can be quoted.